May Economic Background

Global equities continued their April rally into May following March’s 5.6% drawdown initiated by the outbreak of conflict in the Middle East. The equity rally was driven in part by the market’s optimism of a potential diplomatic resolution between the US and Iran, but it drew a stark contrast with the reality of ever-deepening supply shortages in the global oil markets, particularly across Asia.

Global bond markets returned a modest 1.2%, partially recovering from pullbacks of 1.2% and 1.7% in March and April, respectively. Sticky inflation and expectations of higher interest rates throughout 2026 continued to weigh on bond markets, with US treasuries selling off and yields on long term UK borrowing hitting multi-decade highs.

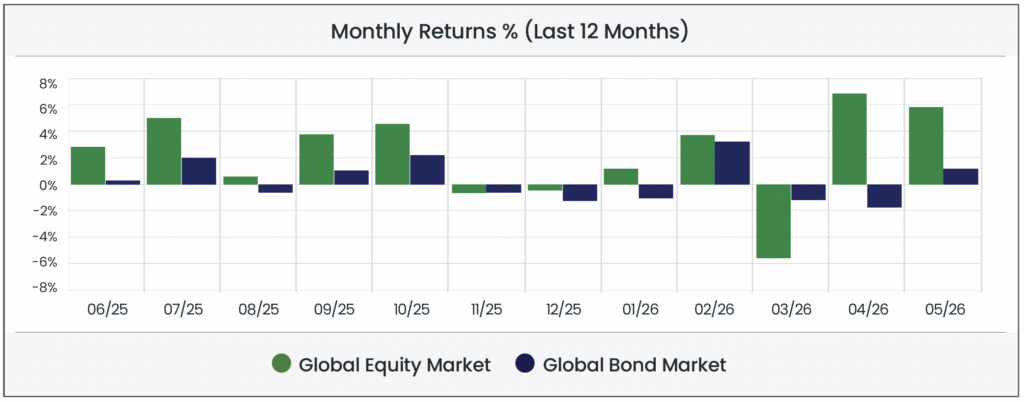

Equity & Bond Performance (Last 3 Months)

Source: Morningstar (Morningstar Global Markets; Bloomberg Global Agg). Data as of 31/05/2026 in GBP terms.

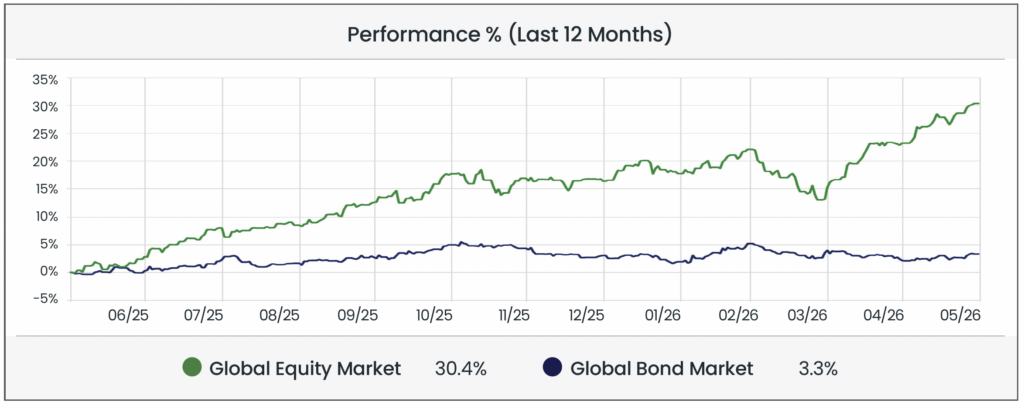

Source: Morningstar (Morningstar Global Markets; Bloomberg Global Agg). Data as of 31/05/2026 in GBP terms.

Source: Morningstar (Morningstar Global Markets; Bloomberg Global Agg). Data as of 31/05/2026 in GBP terms.

Economic Background

Equity markets rally despite deepening shortages in energy and commodities

Global equity markets delivered a strong performance in May, defying (or at least delaying) earlier predictions of market corrections.

In the US, the S&P 500, Nasdaq Composite, and Dow Jones all hit all-time highs on the final trading day of the month, with the growth led predominantly by the technology sector where the “Magnificent Seven”, buoyed by earnings reports which exceeded Wall Street’s expectations, led the way despite all seven underperforming the S&P 500 at multiple points earlier in the year.

Optimism around artificial intelligence (AI) broadened significantly beyond the US too. South Korea’s Kospi index overtook India’s stock market to become the sixth largest in the world, propelled to new heights by SK Hynix and Samsung, both of which joined Taiwan’s TSMC as Asia’s first trillion (US) dollar companies. Japan’s Nikkei 225 rose sharply too, with heavily AI-invested Softbank ending Toyota’s decades long reign as Japan’s most valuable company. The UK’s FTSE 100 was a notable laggard, battling more pessimistic sentiment on the energy front, and lacking any significant exposure to the AI frenzy.

One of the key driving forces behind the widespread rally was the market’s apparent conviction that a tenuous ceasefire between the US and Iran would give way to a more embedded and longstanding diplomatic agreement and that the Strait of Hormuz would reopen relatively quickly. By the end of May, this still hadn’t happened.

Though markets continued to price in a reopening of the Strait and a normalisation of supply chains quickly, even if that were to be the case experts indicated that supply within the global oil system is already at levels which may well take several months to recover from, and economists warned of slowdowns in global economic growth. The Executive Director of the International Energy Agency (IEA) presented a stark warning, that the combined impacts of the situation in the Middle East is “the greatest threat to global energy in history”. Whilst the immediate fallout from rising fuel prices remained reasonably contained in the West by drawdowns in strategic petroleum reserves, the spreading energy disruption is most apparent across Asia, risking supply chains on which western developed markets are critically dependent.

Gilt yields hit long-term highs

The UK gilt market endured a turbulent month in May, rocked by two simultaneous shocks. The ongoing Middle East conflict had already driven 10-year yields to almost 5% in March – their highest since 2008 – as surging energy prices forced markets to price in Bank of England rate hikes, a reversal from the pre-conflict expectations of rate cuts throughout 2026.

Into that fragile economic backdrop then came a domestic political crisis. Disastrous local election results for the Labour party – losing 1498 council seats and 38 local councils, with votes shifting to Reform UK and the Green Party – pushed long-term borrowing costs to their highest in nearly 20 years, as markets worried that a change in leadership could loosen fiscal discipline.

Partial relief came in the second half of the month. Potential Labour leadership challenger Andy Burnham’s commitment to maintain existing fiscal rules, combined with easing oil prices, triggered a rally in gilt prices, with yields dropping around 30 basis points (0.3%) on the 30-year gilt in a single session.

SEC prospectus submitted for all-time largest IPO

In May, one of the most anticipated initial public offerings (IPOs) in history moved from speculation to reality and is set to alter the composition of the major US indices more quickly than initially expected, impacting passive investors around the world.

On 20th May, Elon Musk’s SpaceX publicly filed its offering prospectus with the Securities and Exchange Commission (SEC), allowing the public to see for the first time the audited financial accounts of the rocket company, whose stated corporate strategies over the coming years include orbital and lunar infrastructure, interplanetary colonisation, and “extending the light of consciousness to the stars”. The company posted a loss in 2025 of $4.9 billion from a revenue of $18.7 billion, a revenue which means it will likely be priced on the Nasdaq at a value of around one hundred times revenues, an extraordinarily high valuation.

In what is widely seen a move tailor-made for SpaceX’s offering, the Nasdaq index changed its rules at the start of May with regards to how quickly newly public companies can be included in its index, and other indices are also considered likely to include the rocket company quickly too. This is significant for millions of investors around the world who passively track large indices like the Nasdaq, because it enforces mechanical inclusion of the stock into passive investment vehicles.

AI giants OpenAI and Anthropic are also likely to have similarly large IPOs later in the year, and some analysts have warned that the flurry of activity could deepen concerns around market concentration and the potential technology bubble.

For financial professionals only.

Disclaimer

We do not accept any liability for any loss or damage which is incurred from you acting or not acting as a result of reading any of our publications. You acknowledge that you use the information we provide at your own risk.

Our publications do not offer investment advice and nothing in them should be construed as investment advice. Our publications provide information and education for financial advisers who have the relevant expertise to make investment decisions without advice and is not intended for individual investors.

The information we publish has been obtained from or is based on sources that we believe to be accurate and complete. Where the information consists of pricing or performance data, the data contained therein has been obtained from company reports, financial reporting services, periodicals, and other sources believed reliable. Although reasonable care has been taken, we cannot guarantee the accuracy or completeness of any information we publish. Any opinions that we publish may be wrong and may change at any time. You should always carry out your own independent verification of facts and data before making any investment decisions.

The price of shares and investments and the income derived from them can go down as well as up, and investors may not get back the amount they invested.

Past performance is not necessarily a guide to future performance.

What else have we been talking about?

- Q2 Market Review 2026

- June Market Review 2026

- There’s More to Diversification Than Buying the Index

- Volatility in SpaceX Show IPO Rules Exist for a Reason

- Here’s what happens when a $1tn company joins the index

Blog Post by Jonathan Simpson

Investment Support Analyst at ebi Portfolios