June Economic Background

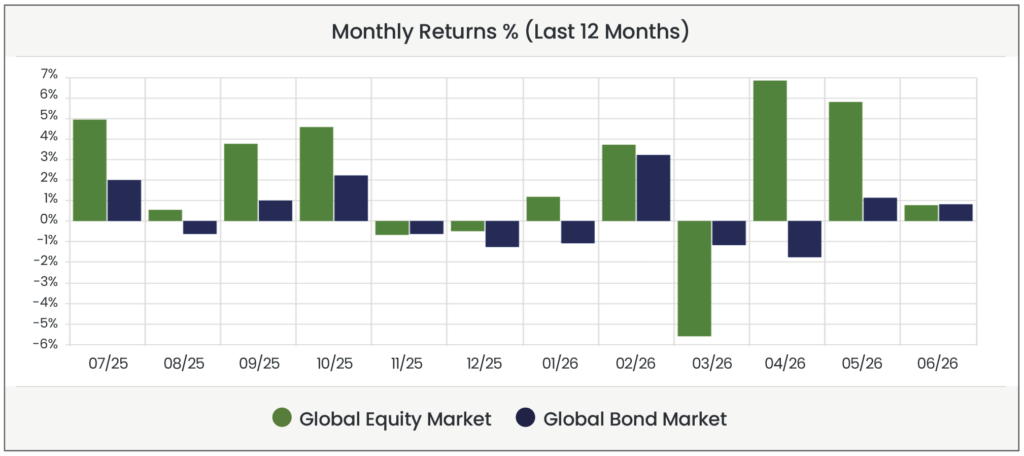

Global equity markets had a disappointing June following two relatively strong prior months. Market weakness in the first half of the month was followed by a recovery after the US and Iran reached a memorandum of understanding to extend an existing ceasefire, and finished the month 0.78% higher. Despite this slowdown in performance relative to the previous months, equities still had a standout second quarter, rising 14% overall. June also saw bonds outperform equities for the first time since March, climbing 0.84% as fixed income products were buoyed by the expectation of lower inflation and lower interest rates ahead.

Equity & Bond Performance (Last 3 Months)

Source: Morningstar (Morningstar Global Markets; Bloomberg Global Agg). Data as of 30/06/2026 in GBP terms.

Source: Morningstar (Morningstar Global Markets; Bloomberg Global Agg). Data as of 30/06/2026 in GBP terms.

Source: Morningstar (Morningstar Global Markets; Bloomberg Global Agg). Data as of 30/06/2026 in GBP terms.

Economic Background

Middle East ceasefire sends oil lower and equities higher

The Presidents of the United States and Iran signed a memorandum of understanding to extend the existing ceasefire for 60 days, while cooperating to reopen the Strait of Hormuz and lift economic sanctions. The 14-point agreement included a US commitment of $300 billion for the reconstruction and economic development for Iran, and a reaffirmation from Iran that it will not procure or develop nuclear weapons.

Market sentiment improved markedly in the second half of the month following the agreement as the likelihood of prolonged supply disruption in global energy and commodity markets diminished. Oil prices fell particularly sharply, with Brent crude slipping below $75 a barrel by the end of June from as high as $110 during the conflict.

Global equity markets, which had dipped in the first part of June, reversed course to end the month 0.78% up, suggesting increased confidence amongst investors that the ceasefire would hold and that Strait traffic would normalise, despite Israel’s continued military strikes in Lebanon threatening the peace process. Travel and airline stocks rose in particular, joined by technology growth stocks both in the US and more broadly across tech-weighted Asian markets. The US tech-heavy Nasdaq gained around 3% on the day of the announcement, as potential inflation relief improved expectations for rate cuts. In general, growth equities move inversely to rates, as their potential future earnings are discounted by less. Japan, which is highly reliant on imports to meet its domestic energy demand (and heavily dependent on the Middle East specifically) saw its leading stock index – the Nikkei 225 – jump around 5.6% in June. Meanwhile in Europe the STOXX 600 rose by 1.6% as companies were seen benefitting from lower oil prices. The UK’s FTSE 100 climbed, led mostly by gains in defence and financial stocks, achieving a sixth consecutive quarterly gain. The resignation of the Prime Minister did little to impact valuations, as markets had mostly priced in the event over the prior weeks and months.

Despite June’s apparent progress in negotiations, the global economy is far from fully recovered. Though commercial shipping via the Strait of Hormuz began to rebound in the days following the memorandum, it slowed towards the end of the month as Washington and Tehran exchanged strikes in the region. Iran also reportedly rejected an effort by Oman and France to de-mine the Strait. The UN’s Trade and Development Agency warned that supply chains and food systems would take longer to recover than energy deliveries.

Hawkish stances from the major central banks in June

June saw the US Federal Reserve (Fed) and the Bank of England (BoE) both taking hawkish postures, while the European Central Bank (ECB) went a step further and hiked rates. This was the first rate increase for the ECB in nearly three years, lifting the main deposit facility rate from 2% to 2.25%, with more hikes expected in the coming months. The decision was a clear and explicit response to Middle East inflationary pressures, with President Christine Lagarde stating that “the full implication of the war for medium-term inflation… will depend on the intensity and duration of the energy price shock… and its indirect and second-round effects”. Eurozone inflation continues to cause concern across the continent, rising to 3.2% in May from 3% in April.

The BoE’s Monetary Policy Committee held its key rate steady at 3.75% – but the dissenting voice grew louder with two members voting to hike rates to 4%. At the previous meeting, there was only one vote for a hike. Concern remains about a lagging energy supply shock, and while Governor Andrew Bailey called the drop in oil prices “encouraging’, he also noted that the conflict in the Middle East had left “inflationary pressures in the pipeline”. The pace of general price increases is already well above the UK’s 2% target, but projections have been lowered since the beginning of the war.

Across the Atlantic new Fed Chair Kevin Warsh began his tenure in charge of the world’s largest central bank, with his committee opting to hold benchmark rates unchanged between 3.5% and 3.75%. Members weren’t unified in their decision, with some voting to raise rates to quell inflation which is still above target at 3.8%. The decision is viewed by some as reassuring, given that President Trump had put tremendous political pressure on Warsh’s predecessor Jerome Powell to take on a more dovish stance, and had made it clear that his expectations were the same for Warsh. A Trump appointee, there had been concerns that Warsh might recklessly lower rates despite the realities of the US economy. This – at least in June – did not transpire.

Weak UK economic growth persists

Figures released in June showed that the UK economy (as measured by gross domestic product) shrank by 0.1% in April, following consecutive months of slight growth. Unemployment – a strong indicator of poor economic health – is forecast by the British Chamber of Commerce (BCC) to reach 5.2% in 2026, and the BCC also noted that growth was projected to remain subdued throughout 2026 and 2027.

There were fears that Andy Burnham’s victory in the Makerfield by-election (and his apparent coronation as Prime Minister later this year) could trigger volatility in the bond markets, despite his recent commitment to stick to the Labour party’s existing fiscal rules. Indeed, the ten-year gilt yield climbed by more than 0.08% in the aftermath of Burnham’s election to over 4.83%, with the two-year and thirty-year bond yields also moving higher. However, the net impact of the election was less than many expected, and it may be that investors are waiting for Labour’s autumn budget to decide how they feel about the UK’s new leadership.

For financial professionals only.

Disclaimer

We do not accept any liability for any loss or damage which is incurred from you acting or not acting as a result of reading any of our publications. You acknowledge that you use the information we provide at your own risk.

Our publications do not offer investment advice and nothing in them should be construed as investment advice. Our publications provide information and education for financial advisers who have the relevant expertise to make investment decisions without advice and is not intended for individual investors.

The information we publish has been obtained from or is based on sources that we believe to be accurate and complete. Where the information consists of pricing or performance data, the data contained therein has been obtained from company reports, financial reporting services, periodicals, and other sources believed reliable. Although reasonable care has been taken, we cannot guarantee the accuracy or completeness of any information we publish. Any opinions that we publish may be wrong and may change at any time. You should always carry out your own independent verification of facts and data before making any investment decisions.

The price of shares and investments and the income derived from them can go down as well as up, and investors may not get back the amount they invested.

Past performance is not necessarily a guide to future performance.

What else have we been talking about?

- Q2 Market Review 2026

- June Market Review 2026

- There’s More to Diversification Than Buying the Index

- Volatility in SpaceX Show IPO Rules Exist for a Reason

- Here’s what happens when a $1tn company joins the index

Blog Post by Jonathan Simpson

Investment Support Analyst at ebi Portfolios