Here’s what happens when a $1tn company joins the index

The current wave of mega-IPOs is reviving a familiar concern about passive and rules-based investing: that broadly diversified portfolios would be forced to buy fashionable new stocks in vast quantities just as excitement peaks. The reality is more disciplined and more interesting than that.

The introduction of SpaceX, OpenAI and Anthropic to public markets is sharpening an old worry among widely diversified investors.

When these companies list at valuations of $1 trillion or more, does a passive investor simply inherit that headline size inside the portfolio? Worse, does the portfolio have to buy that full exposure as though all outstanding shares were publicly available on day one, just as excitement around the listing peaks, potentially blowing up their portfolios like a space rocket on failed launch?

Not quite.

A $1 trillion valuation is not the same thing as a $1 trillion index weight. For diversified investors, the more important question is not what a company is worth on paper, but how much of it the market can actually buy.

The mitigation lies in the machinery of index investing: the rules that decide when a new company becomes part of the market, how much of it an index fund has to own, and whether different portfolio designs absorb that exposure in the same way.

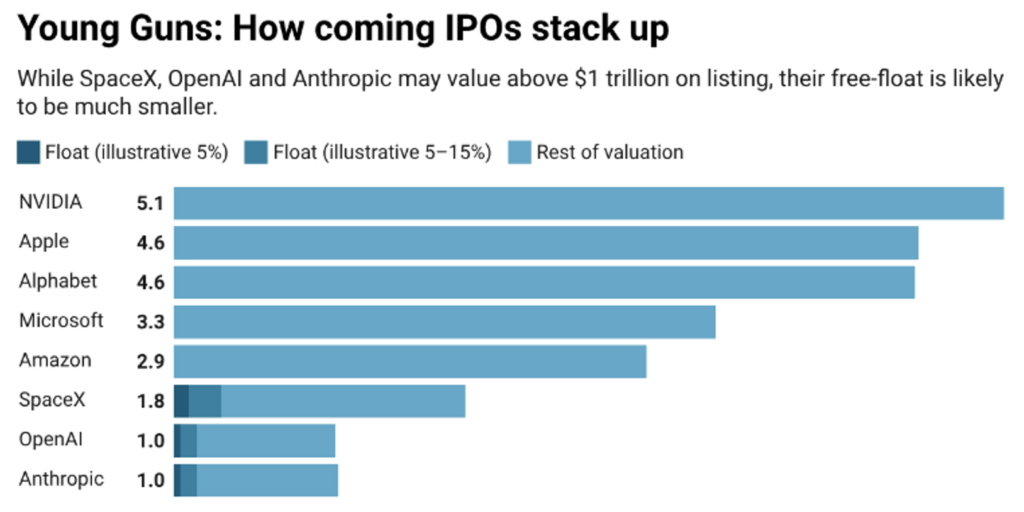

The gap between what a company is worth and how much of it an index actually holds is perhaps the most misunderstood part of the story. Mega-IPOs often make only a small proportion of their shares available to public investors at listing. Founders, early investors and employees may remain locked in. Strategic holders may not sell. The publicly tradeable slice can be much smaller than the total company value implies.

ㅤ

On float-adjusted indices, that matters directly. Index weight is based on the shares actually available to investors, not the entire theoretical value of the company. A business valued at $1tn but with only a modest public float does not enter the index as if the whole $1tn were freely tradeable. Its initial weight is reduced, and later increases tend to come in stages as lock-ups expire and more shares become available.

ㅤ

Listed company market capitalisations: companiesmarketcap.com, as at 1 June 2026; figures move daily. Private company figures are reported valuation estimates, not market capitalisations: SpaceX ~$1.75-2tn (IPO target); OpenAl ~$1tn (reported IPO scenario; last private round $852bn, March 2026); Anthropic $965bn (funding round, May 2026). Free-float figures are illustrative. SpaceX’s ~5% reflects reporting of a ~$70-75bn raise against its target valuation; OpenAl and Anthropic have not disclosed offering sizes, so the 5-15% band shown for them is assumption, not data.

Chart: ebi Portfolios – Ed van der Walt. Created with Datawrapper

Where the current crop is concerned, SpaceX has gone first: it priced at $135 a share and began trading on Nasdaq on 12 June at a valuation near $1.77tn, having raised roughly $75bn. Only about 4% of its shares floated, making it a textbook case of the gap. Anthropic, valued at $965bn in its May 2026 round, filed confidentially on 1 June, and OpenAI (valued at $852bn, with reports of a possible ~$1tn listing) followed on 8 June, but neither has set a share count or price, so their floats cannot yet be estimated.

But the Nasdaq-100 is not the whole market.

MSCI and FTSE Russell operate under different rules, with their own tests around size, liquidity, seasoning and free float. Standard listings generally face a waiting period before they are considered at a scheduled index review, while only the largest IPOs qualify for early inclusion. The precise thresholds differ, but the principle is the same: index providers are not simply adding every new company immediately because it has become fashionable.

Most rules-based portfolios do not track “the market” through a single index provider, a single benchmark or a single inclusion mechanism. They are built from multiple funds, tracking different indices, with different eligibility screens and different construction methods. So the practical exposure to a mega-IPO depends on where the company lists, which index admits it, when it is eligible, how much free float is available, and which funds in the portfolio actually track that benchmark.

The Aramco lesson

Saudi Aramco is the cleanest recent reminder that headline size and index weight are not the same thing.

When Aramco listed in December 2019, it was briefly the largest listed company in the world. MSCI put its full-company market capitalisation at roughly $1.88tn, but only about 0.5% of the company was freely available to public investors. On inclusion, MSCI estimated its weight at just 0.16% of the MSCI Emerging Markets Index and 0.02% of MSCI ACWI, despite a much larger weight in the domestic Saudi index.

The point is not that Aramco is a perfect guide to the next mega-IPO. It is that float-adjusted index weights reflect the investable market – the shares actually available to buy – not the full theoretical value of a business.

Most rules-based portfolios do not track “the market” through a single index provider, a single benchmark or a single inclusion mechanism. They are built from multiple funds, tracking different indices, with different eligibility screens and different construction methods. So the practical exposure to a mega-IPO depends on where the company lists, which index admits it, when it is eligible, how much free float is available, and which funds in the portfolio actually track that benchmark.

Not all passive exposure is the same

“Passive” is not a single portfolio design.

A broad market-cap tracker is the most mechanically exposed. If the benchmark admits a new company, the fund generally needs to hold it in line with the index methodology. That is the cleanest expression of market ownership. But even here, specifics matter. Generally MSCI applies a longer waiting period, and a higher size bar for early inclusion, than FTSE does, though for the very largest listings that bar is cleared either way.

Other rules-based strategies behave differently still. ESG-screened or optimised funds may not hold every parent-index constituent at its market weight, which can dampen or delay the inclusion of a new stock.

Factor-tilted funds add another layer. A factor strategy doesn’t hold a company merely because it is large. It does so to achieve exposure to characteristics such as value, quality, momentum, minimum volatility or size, within a rules-based framework. A newly listed, high-profile company will only be useful to the strategy if it helps meet those objectives. In many cases, the methodology will also rely on scheduled reviews rather than immediate early inclusion.

That is not a guarantee that factor or optimised strategies avoid IPOs. Yet compared with a plain market-cap tracker, a rules-based optimisation process can make the portfolio less mechanically exposed to the first wave of index inclusion, and because it only wants a stock to the extent that stock improves its objective, it can decline or limit a new listing that does not earn its place. So the question is not only the size of the forced purchase, but whether the construction is obliged to make it at all.

Diversification remains the main defence

Even where a mega-IPO enters an index, the portfolio-level impact is diluted by breadth.

A globally diversified equity allocation can hold thousands of securities across regions, sectors and styles. A single new company can matter a great deal to its early investors, to the index provider, and to the funds that must trade around the event. It does not follow that it becomes a dominant risk in a diversified portfolio.

The discipline of evidence-based investing is not built on predicting which IPOs will disappoint or which will compound for decades. It is built on owning broad markets efficiently, controlling costs, diversifying across sources of return, and resisting event-driven bets that depend on being smarter than the next buyer or seller.

So the right position is not that these portfolios are immune from IPO risk. They are not: once a company becomes a material part of the investable market, index-led investors will usually own it in some form. The point is that the exposure is governed by rules rather than excitement, filtered through index methodology, constrained by free float, moderated by portfolio construction and diluted through diversification.

That is what discipline looks like in practice: not an attempt to forecast whether the next mega-IPO will soar or disappoint, but a process that keeps any single listing in its proper place.

Ed van der Walt, CFA – Assistant Portfolio Manager, ebi

Joshua Clarke, CFA – Portfolio Manager, ebi

Jonathan Griffiths, CFA – Head of Investment, ebi

This article was first published on FT Adviser on 17 June 2026.

Sources: Nasdaq, FTSE Russell (LSEG) and MSCI index methodology documents; MSCI, “Aramco IPO shows importance of timely index inclusion” (Aramco free float and index weights); Reuters (Aramco MSCI Saudi Arabia weight). Listed company market capitalisations: companiesmarketcap.com, as at 1 June 2026. Private company valuations and offering details: CNBC, Reuters, Bloomberg and TechCrunch reporting, May–June 2026 (SpaceX ~$1.77tn valuation at ~$135/share and ~$75bn raise, expected to list June 2026; Anthropic $965bn May 2026 round, confidential IPO filing 1 June 2026; OpenAI $852bn March 2026 round). ebi portfolio composition data: Morningstar Direct.

For financial professionals only.

Disclaimer

We do not accept any liability for any loss or damage which is incurred from you acting or not acting as a result of reading any of our publications. You acknowledge that you use the information we provide at your own risk.

Our publications do not offer investment advice and nothing in them should be construed as investment advice. Our publications provide information and education for financial advisers who have the relevant expertise to make investment decisions without advice and is not intended for individual investors.

The information we publish has been obtained from or is based on sources that we believe to be accurate and complete. Where the information consists of pricing or performance data, the data contained therein has been obtained from company reports, financial reporting services, periodicals, and other sources believed reliable. Although reasonable care has been taken, we cannot guarantee the accuracy or completeness of any information we publish. Any opinions that we publish may be wrong and may change at any time. You should always carry out your own independent verification of facts and data before making any investment decisions.

The price of shares and investments and the income derived from them can go down as well as up, and investors may not get back the amount they invested.

Past performance is not necessarily a guide to future performance.

What else have we been talking about?

- Q2 Market Review 2026

- June Market Review 2026

- There’s More to Diversification Than Buying the Index

- Volatility in SpaceX Show IPO Rules Exist for a Reason

- Here’s what happens when a $1tn company joins the index