April Economic Background

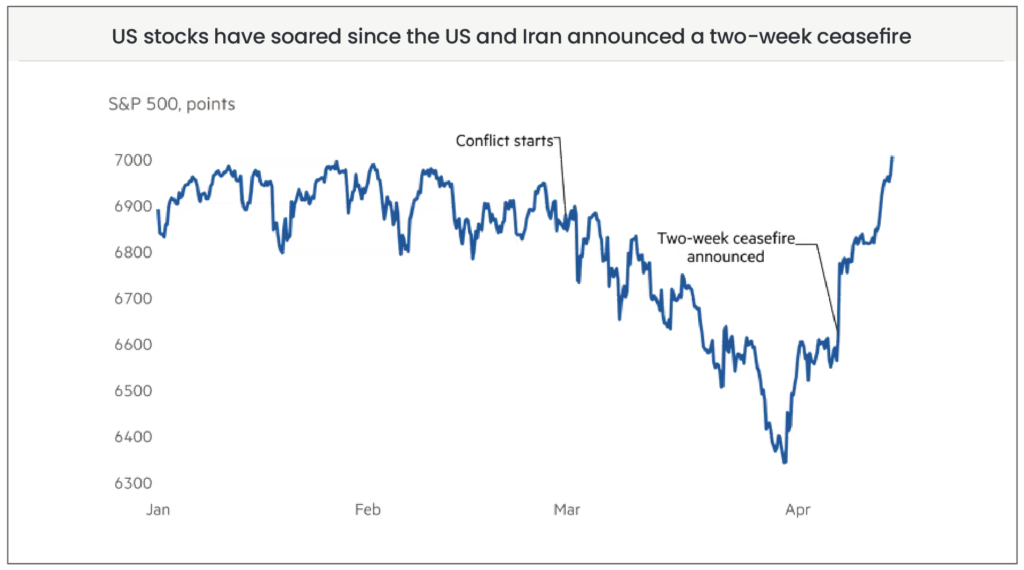

April saw a strong rebound from March’s sharp sell-off, as easing tensions in the Middle East and resilient corporate earnings helped restore confidence across global equity markets. Global equities returned 6.9% for the month, more than recouping March’s losses, while global bonds returned -1.7% as bond yields continued to rise on inflation concerns. The turnaround was sparked early in the month, when President Trump suggested the war in Iran could end within “two or three weeks”, followed by a US-Iran ceasefire on 8th April that was due to reopen the Strait of Hormuz. Oil prices tumbled and risk assets surged, with the S&P 500 going on to hit record highs in mid-April. However, the rally was softened by renewed volatility late in the month, as peace talks broke down, the US imposed a naval blockade of Iran, and oil prices climbed back above $125 a barrel by month-end.

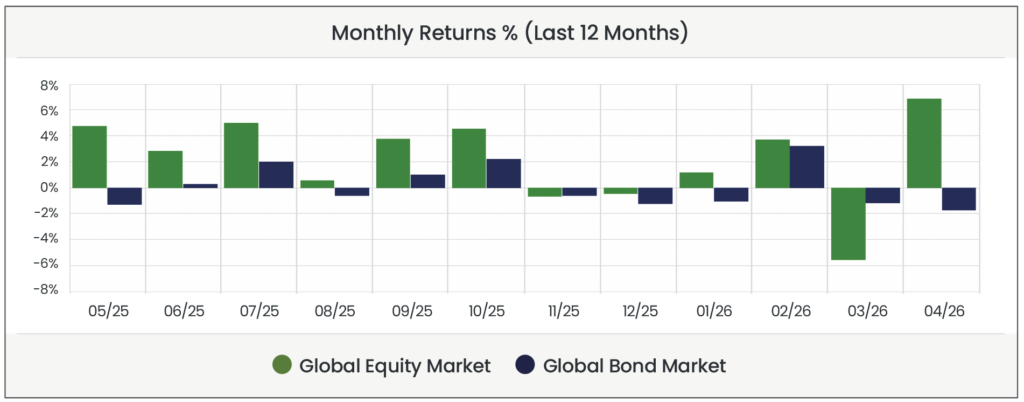

Equity & Bond Performance (Last 3 Months)

Source: Morningstar (Morningstar Global Markets; Bloomberg Global Agg). Data as of 30/04/2026 in GBP terms.

Source: Morningstar (Morningstar Global Markets; Bloomberg Global Agg). Data as of 30/04/2026 in GBP terms.

Source: Morningstar (Morningstar Global Markets; Bloomberg Global Agg). Data as of 30/04/2026 in GBP terms.

Economic Background

Ceasefire hopes give way to renewed tensions

April began on an optimistic footing, with markets rallying after President Trump signalled the US could withdraw from Iran within “two or three weeks”. The diplomatic breakthrough came on 8th April, when the US and Iran agreed a two-week ceasefire that was due to reopen the Strait of Hormuz to shipping traffic. Brent crude tumbled to below $90 a barrel, and European assets rallied sharply on hopes that lower energy costs would ease the inflation outlook and revive the case for interest rate cuts. The Stoxx Europe 600 jumped nearly 4% and Germany’s Dax advanced 5% in a single session. The truce, however, proved fragile. Israeli strikes continued in Lebanon and Iran kept tight control over the Strait of Hormuz, demanding tolls from vessels and limiting traffic. By mid-month, US-Iranian peace talks hosted by Pakistan had collapsed, and Trump announced a US naval blockade of Iranian shipping. Brent surged back above $125 a barrel by month-end (the highest level since 2022) after the US navy seized an Iranian cargo ship in the Gulf of Oman and Trump signalled he would maintain the blockade until Tehran agreed to end its nuclear programme. Yet despite the ongoing fragility and persistent tensions in the Middle East, equity markets brushed aside the geopolitical noise to post strong gains for the month, with major indices recovering well beyond their March losses.

S&P 500 and emerging markets hit record highs

Global equity markets staged a remarkable comeback in April, with both US and emerging market indices reaching record highs by month-end despite the ongoing turbulence in the Middle East. US stocks have soared since the announcement of the US-Iran ceasefire, with the S&P 500 closing above 7,000 for the first time on 15th April. The recovery from the conflict marked one of the sharpest 10-day rebounds for the index in years, as investors shifted their focus from the Middle East energy shock to the prospect of resilient corporate earnings and continued economic growth. The rally was broad-based but led by the technology sector, where renewed enthusiasm around artificial intelligence reignited investor appetite. Emerging market equities also recovered all of their war-related losses to hit a fresh all-time high, propelled by Asian chipmakers that sit at the heart of the AI supply chain. European equities lagged by comparison, weighed down by the region’s high exposure to energy costs and their reliance on Middle Eastern energy imports.

Source: LSEG

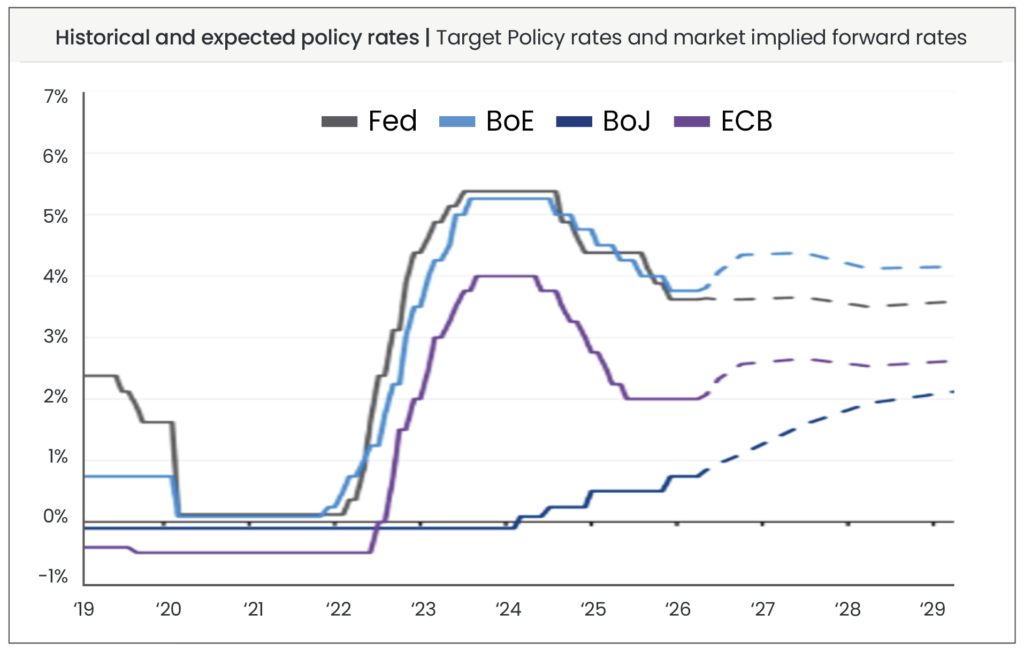

Central banks hold firm as bond yields stay elevated

In contrast to the strength seen in equity markets, global bonds remained under pressure throughout April, returning -1.7% for the month. With energy prices still elevated and the inflation outlook clouded by the ongoing conflict, investors continued to reassess how quickly central banks would be able to resume cutting interest rates, a sharp shift from the optimism that had prevailed at the start of the year.

Against this backdrop, major central banks held rates steady in April. The Bank of England (BoE) kept its key rate at 3.75% in an 8-1 vote, with chief economist Huw Pill the lone dissenter calling for an immediate quarter-point rise. The European Central Bank (ECB) also held rates steady at 2%, while the Bank of Japan (BoJ) kept its benchmark rate at 0.75% but raised its inflation forecast for the current fiscal year sharply to 2.8%, reflecting Japan’s heavy reliance on Middle Eastern oil imports. Inflation data through the month justified the cautious tone: the UK Consumer Price Index (CPI) rose to 3.3% in March, while Eurozone inflation climbed to 3% in April, both well above the 2% targets.

Bond prices and yields move inversely, so as investors demanded higher yields to compensate for the risk of persistent inflation, bonds sold off and yields pushed higher. UK 10-year gilt yields touched 5.1% in late April, near their highest level since 2008, while German Bund yields reached their highest since 2011. With oil back above $125 a barrel by month-end, the prospect of meaningful rate cuts in 2026 looked more remote than at any point this year so far, leaving the path for bond markets largely dependent on the eventual resolution of the conflict.

Source: Bank of England (BoE), Bank of Japan (BoJ), Bloomberg, European Central Bank (ECB), Federal Reserve (Fed), OECD, J.P. Morgan Asset Management. Guide to the Markets – U.S. Data are as of April 30, 2026.

For financial professionals only.

Disclaimer

We do not accept any liability for any loss or damage which is incurred from you acting or not acting as a result of reading any of our publications. You acknowledge that you use the information we provide at your own risk.

Our publications do not offer investment advice and nothing in them should be construed as investment advice. Our publications provide information and education for financial advisers who have the relevant expertise to make investment decisions without advice and is not intended for individual investors.

The information we publish has been obtained from or is based on sources that we believe to be accurate and complete. Where the information consists of pricing or performance data, the data contained therein has been obtained from company reports, financial reporting services, periodicals, and other sources believed reliable. Although reasonable care has been taken, we cannot guarantee the accuracy or completeness of any information we publish. Any opinions that we publish may be wrong and may change at any time. You should always carry out your own independent verification of facts and data before making any investment decisions.

The price of shares and investments and the income derived from them can go down as well as up, and investors may not get back the amount they invested.

Past performance is not necessarily a guide to future performance.

What else have we been talking about?

- Q2 Market Review 2026

- June Market Review 2026

- There’s More to Diversification Than Buying the Index

- Volatility in SpaceX Show IPO Rules Exist for a Reason

- Here’s what happens when a $1tn company joins the index

Blog Post by Sam Startup

Investment Analyst at ebi Portfolios