What’s been happening – escalating tensions in the Middle East

The current escalation in the Middle East intensified sharply on Saturday 28th February 2026 when Israel and the United States carried out what it called pre-emptive strikes targeting Iranian strategic and military infrastructure. The attacks marked a significant expansion of hostilities between the two regional powers and heightened fears of a broader regional conflict.

The escalation reflects a long-standing rivalry between the two states, shaped by decades of geopolitical competition, regional power struggles, and security concerns. Both countries have been engaged in an ongoing “shadow conflict”, involving proxy groups, cyber operations, and periodic military strikes. Against this backdrop, Israel’s latest operation (conducted as part of a joint campaign with the US) significantly intensified tensions.

The initial strikes reportedly resulted in the death of Iran’s supreme leader Ali Khamenei and several senior military commanders. In retaliation, Iran launched a sustained campaign of missile and drone attacks against Israel and US allies across the Gulf, including Bahrain, Qatar, Kuwait, and the UAE. The conflict has already caused hundreds of fatalities, including civilian and US military casualties.

Beyond direct hostilities, the war has severely disrupted Gulf shipping and trade, with Iran attacking energy infrastructure as an apparent strategic objective. Iran has warned vessels not to transit the Strait of Hormuz, a critical passage for roughly 20% of global oil supplies. Multiple tankers have been attacked, and over 150 vessels have anchored outside the strait as insurers suspended coverage and premiums surged. Shipping operators, including Maersk, have rerouted vessels via longer alternatives such as the Cape of Good Hope. The disruption is already contributing to rising energy prices and heightened global economic uncertainty, with OPEC+ announcing plans to increase oil production in response.

What the impact of this has been on global markets (so far)

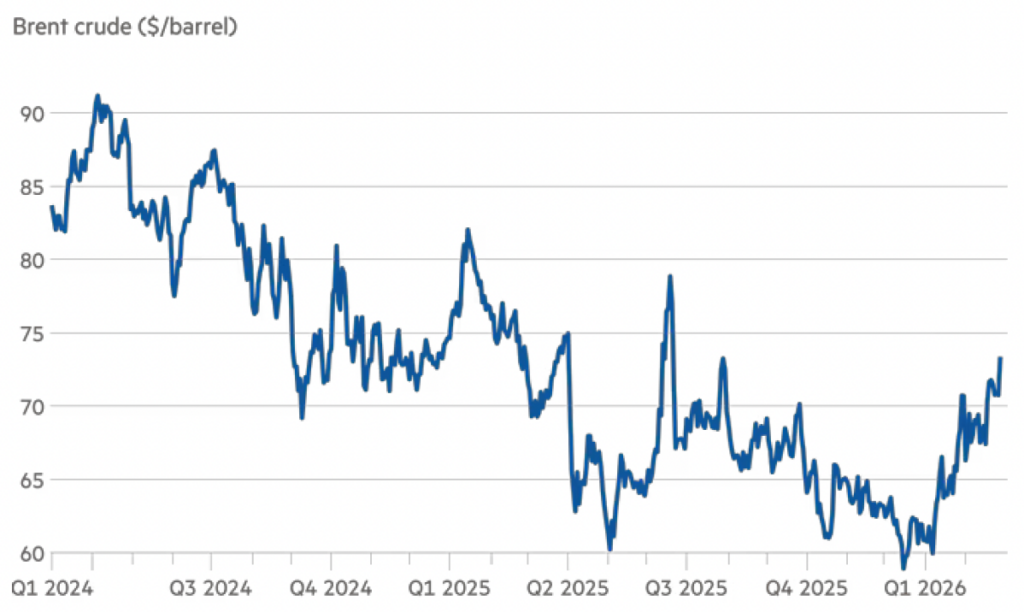

Global markets have reacted sharply to the escalation in the Middle East, with volatility rising across asset classes. Oil prices surged as Iran’s missile and drone strikes, combined with attacks on tankers and the effective closure of the Strait of Hormuz, raised concerns over severe energy supply disruptions. With roughly one in five barrels of global oil transiting the strait, a prolonged shutdown could trigger significant spikes in energy prices. Market participants are closely monitoring whether shipping through the strait can resume safely. If traffic continues and the recent decision by OPEC+ to raise production helps offset supply pressures, the impact on global growth may be contained. Coordinated output increases from other producers could further mitigate potential disruptions.

As markets reopened on Monday 2nd March, oil and gas prices surged and global stocks fell as they came under pressure amid investors reassessing risk. Airlines, logistics, and hotel groups have led declines, with Europe’s benchmark index (Stoxx Europe 600) down 1.5% on Monday, while the US (S&P 500) and UK (FTSE 100) also down 0.4% and 0.6%, respectively (all in local currency terms). Safe haven assets have seen strong demand, with gold, US treasuries, and the US dollar all strengthening.

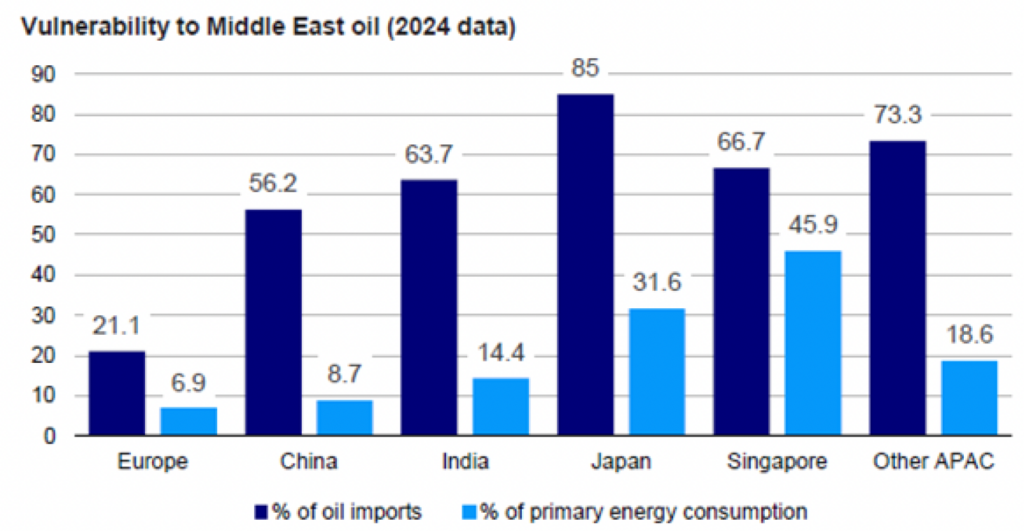

The impact of rising oil prices is unlikely to be felt evenly across the global economy. Countries that rely heavily on imported energy (particularly China, India, and Japan) may be especially vulnerable given their significant dependence on oil supplies from the Middle East. A sustained surge in energy costs would create a significant ripple effect across these economies, raising production and transportation expenses for businesses, increasing operating costs across key industries, resulting in upward pressure on consumer prices. This could ultimately weigh on economic growth, fuel inflation, and lead to tighter financial conditions more broadly.

Source: 2025 Energy Institute Statistical Review of World Energy and Invesco Strategy & Insights. Vulnerability to Middle East Oil shows imports of crude oil and oil products from Middle East countries as a percent of total oil imports and as a percent of primary energy consumption in the countries and areas shown. Data is for 2024.

Oil prices had already risen ahead of the conflict, and further increases could add to inflationary pressures. Higher energy costs are a key driver of inflation and heavily influence central bank decision-making. This could prompt the Federal Reserve and the Bank of England (BoE) to pause their respective rate-cutting cycles if risks of renewed inflation spikes materialise. The BoE’s Monetary Policy Committee has been closely divided in recent decisions, so elevated oil prices could delay planned rate reductions until there is greater clarity on the scale and persistence of the inflationary impact.

Source: LSEG, via the FT

Holding the course

When we look over a longer timeframe (10 years), we can see this volatility is a natural part of investing in the stock market

E.g. Global stock market performance over the past 10 years: +236.3%

Source: Morningstar (Morningstar Global Markets in GBP terms). Data from 03/03/2016 to 02/03/2026.

Volatility is an unavoidable part of investing in global markets, and while steps can be taken to mitigate its impact, it cannot be eliminated entirely. What investors can control is how they respond to short-term turbulence. In situations like this, anxiety and the desire to act quickly can lead to selling assets at a moment when prices may be near temporary lows, potentially undermining long-term portfolio performance. Focusing on a long-term investment plan and the underlying philosophy of the portfolio remains the most reliable strategy.

Market corrections and uncertainty can also create conditions for counterbalancing factors. For instance, heightened concerns over global growth and inflation could influence governments to implement fiscal stimulus measures to ease economies through these more uncertain times.

Remaining disciplined during periods of geopolitical tension and market turbulence allows investors to navigate the uncertainty without taking actions that could be detrimental to longterm goals.

ebi’s portfolios are well – positioned to weather volatile markets

We construct our portfolios to be broadly globally diversified – seeking global exposure in line with the wider market in regional terms, and investing in a wide range of underlying securities, countries, and sectors. Such diversification generally leads to portfolios being well positioned to handle global events and disruption, such as this week’s developments. This is particularly notable in contrast to more concentrated portfolios that might actively seek to trade or time investments in small subsectors of the market, which can then more easily get caught short as the global situation develops and events transpire in ways different to that expected.

In addition, ebi’s factor portfolios (such as our flagship ESG-screened Earth portfolio suite) utilise investment factors as part of their wider investment approach. One of these factors is the ‘Minimum Volatility’ factor, which focuses on investing in companies with lower volatility than the wider market. Utilising this factor can provide protection in volatile markets such as those experienced over last few days, as typically we see higher volatility stocks sell-off to a greater extent than their lower volatility counterparts, and as such a degree of ‘protection’ provided by the Minimum Volatility factor tilt within the factor portfolios. Alongside this, it is important to zoom out and put the short-term market volatility we’re witnessing in the context of longer-term investment performance.

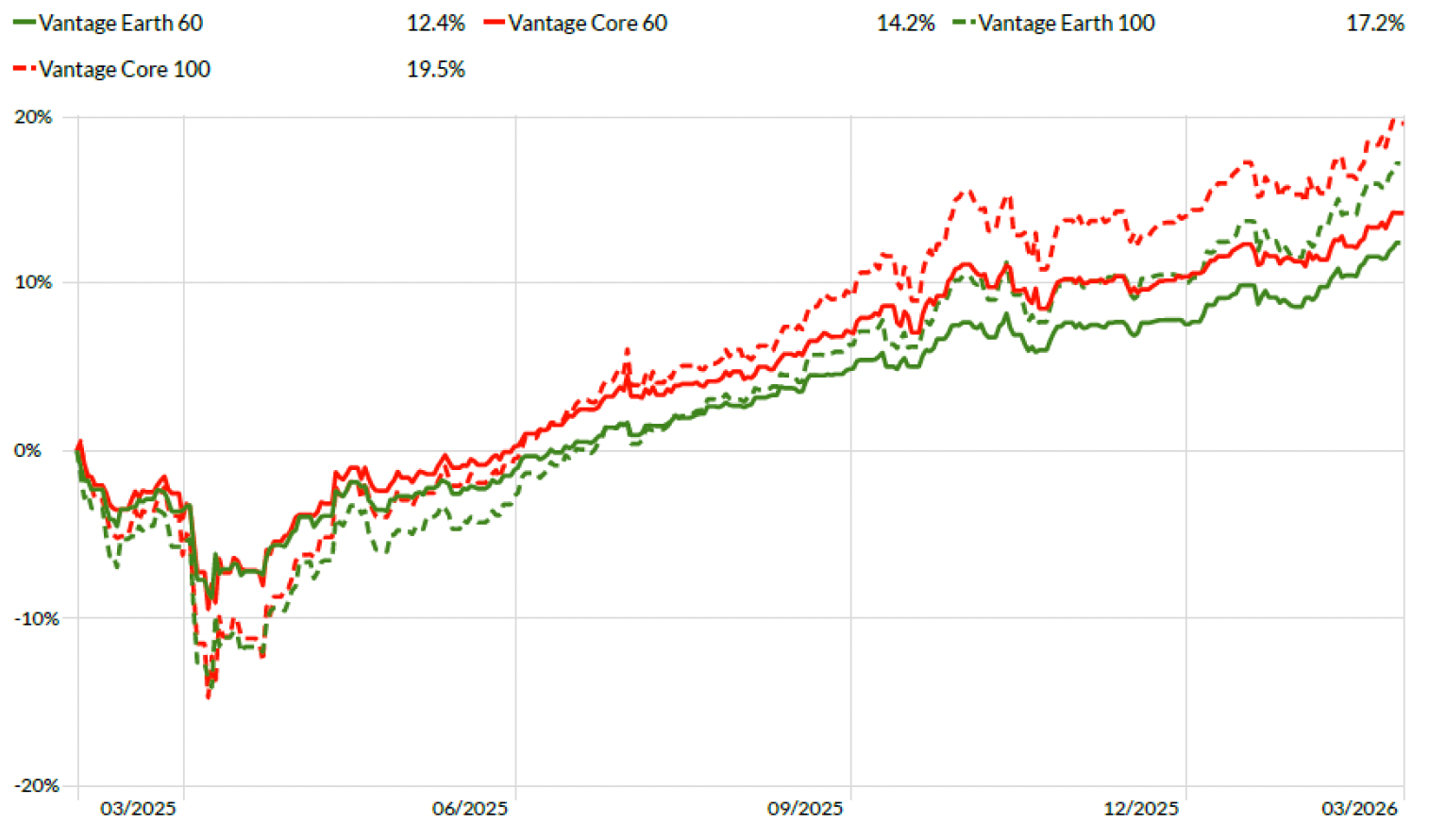

More specifically, over the 12 months to close-of-business on 2nd March 2026 (the latest available data-point), we have seen the following strong returns from some of our main portfolios (all in GBP terms):

• Core 100 (100% equity, market-tracking portfolio): +19.5%

• Core 60 (60% equity: 40% fixed income, market-tracking portfolio): +14.2%

• Earth 100 (100% equity, ESG-screened and factor-tilted portfolio): +17.2%

• Earth 60 (60% equity: 40% fixed income, ESG-screened and factor-tilted portfolio): +12.4%

Source for ebi portfolio data: Morningstar, shown in GBP terms, extracted 02/03/2026.

Source: Morningstar (ebi Earth and Core portfolios in GBP terms). Data from 03/03/2025 to 02/03/2026.

Role of fixed income

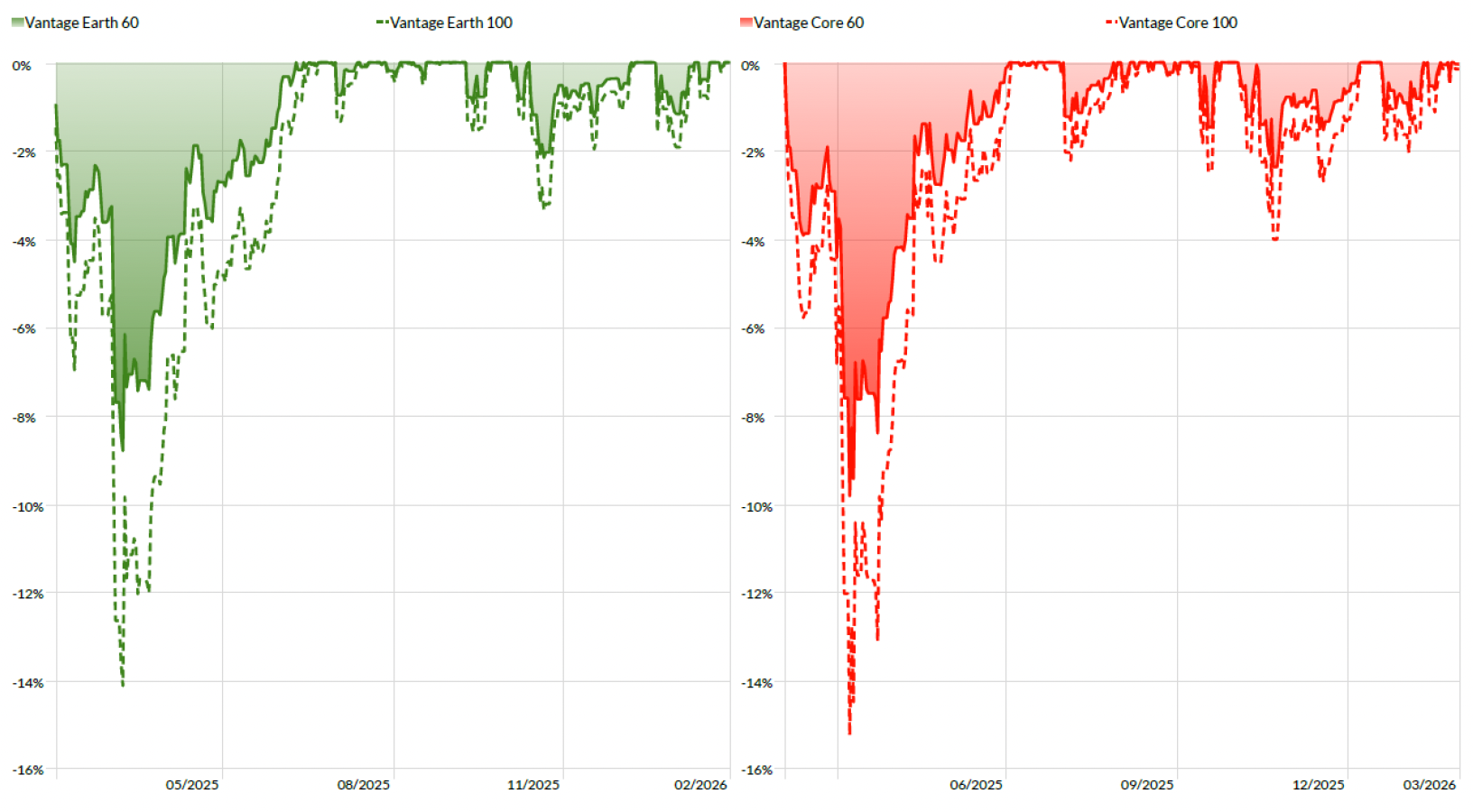

Importantly, fixed income is also serving its role of providing protection in our portfolios, precisely for events such as these, as indicated by the smaller drawdown periods exhibited in the 60% equity portfolio versus the 100% equity portfolio.

Drawdown over the last 12 months: 60/40 portfolio v Equity portfolio

Source: Morningstar (ebi Earth and Core portfolios in GBP terms). Data from 03/03/2025 to 02/03/2026.

While there is no doubt that this week’s events are of geopolitical and economic significance, they do not result in any fundamental changes to the way in which we invest. Namely, we create globally diversified portfolios, using a buy-and-hold approach built on the foundation of comprehensive strategic asset allocations. We maintain these over the long-run, rather than adopting a short-term tactical approach seeking to outperform markets over the short-run. While current events may not be the end of market volatility, our long-term investment approach means that no major changes are either needed nor desired during these times, particularly given the risks that such short-term actions could lead to (for example our active peers may be tempted to make reactionary changes to their portfolios during these times, but time and market pressure can lead to poor investment decisions, and sub-optimal market timing). Instead, we maintain a close eye on global developments, observing announcements, reactions, and investment markets as they play out, specifically with a view to the long-term.

Nonetheless, if you have any specific follow-up questions then please don’t hesitate to reach out to your usual ebi representative or by emailing enquiries@ebi.co.uk.

For financial professionals only.

Disclaimer

We do not accept any liability for any loss or damage which is incurred from you acting or not acting as a result of reading any of our publications. You acknowledge that you use the information we provide at your own risk.

Our publications do not offer investment advice and nothing in them should be construed as investment advice. Our publications provide information and education for financial advisers who have the relevant expertise to make investment decisions without advice and is not intended for individual investors.

The information we publish has been obtained from or is based on sources that we believe to be accurate and complete. Where the information consists of pricing or performance data, the data contained therein has been obtained from company reports, financial reporting services, periodicals, and other sources believed reliable. Although reasonable care has been taken, we cannot guarantee the accuracy or completeness of any information we publish. Any opinions that we publish may be wrong and may change at any time. You should always carry out your own independent verification of facts and data before making any investment decisions.

The price of shares and investments and the income derived from them can go down as well as up, and investors may not get back the amount they invested.

Past performance is not necessarily a guide to future performance.

What else have we been talking about?

- Q2 Market Review 2026

- June Market Review 2026

- There’s More to Diversification Than Buying the Index

- Volatility in SpaceX Show IPO Rules Exist for a Reason

- Here’s what happens when a $1tn company joins the index