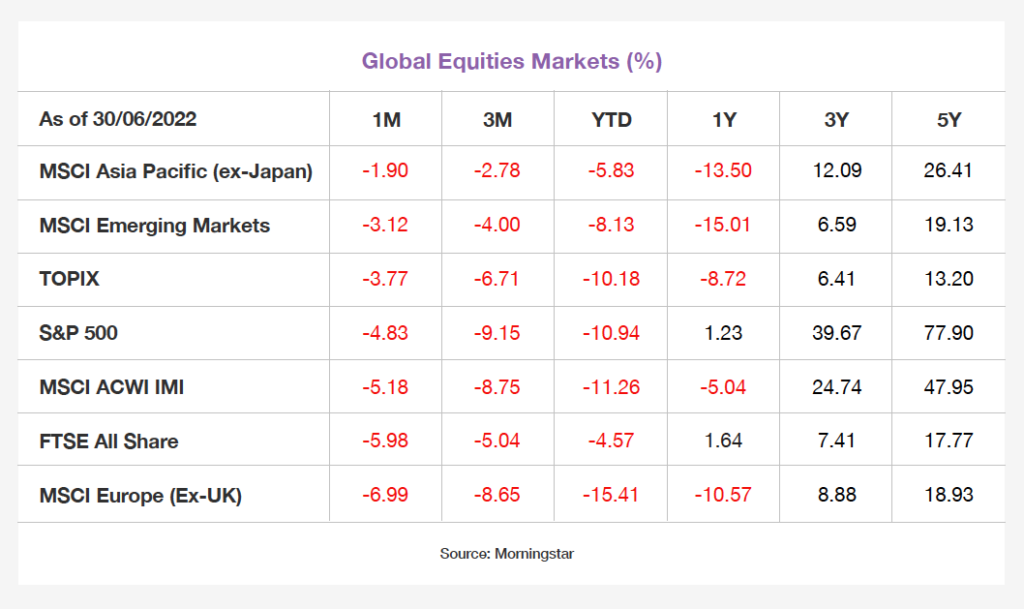

Overall Market Backdrop for June

- Bear markets continued to run in June with all Global markets ending in the red zone fuelled by growth concerns, inflation and volatility.

- Central banks are showing a united front in having a hawkish stance to battle inflation.

- While the US 10-Year Treasury yields did end up higher at the end of the month, there was some resistance mid-month after investment sentiment switched and investors started buying the bond.

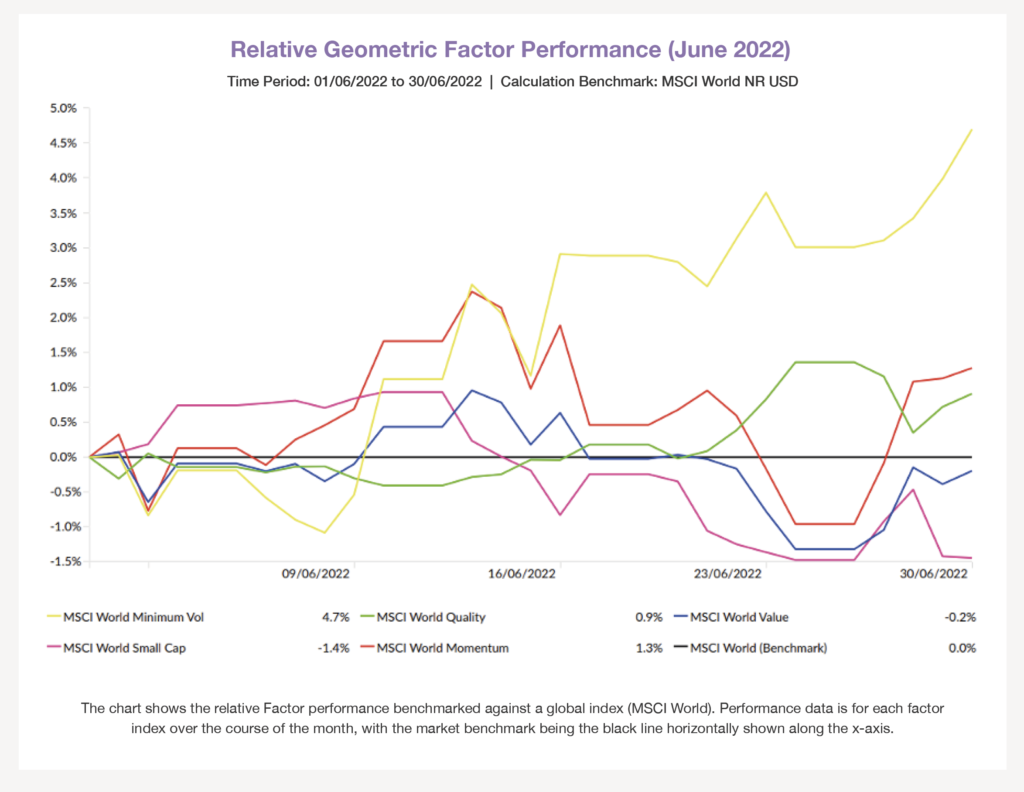

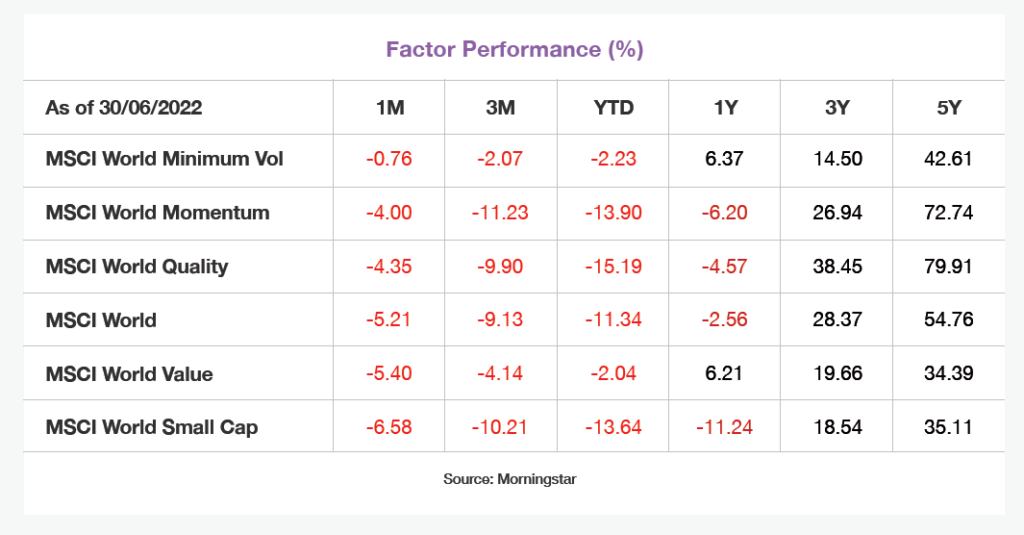

- Minimum Volatility has been the best performing factor for June.

Drivers of Market Conditions in June

- Equity market volatility was common in every region in June, with the VIX index increasing by approximately 10% by the end of the month. US investors once again had to contend with another strong US inflation print. US equities had to deal with threats from multiple directions with central bank tightening, persistent inflation, and higher sovereign yields continuing to drive down the S&P 500. The only respite US equities had was mid-month when Fed Chair Powell went on to give a hawkish Congressional testimony. This was only a temporary bounce back however with recession fears taking hold at the end of the month which once again lowered investor optimism. The S&P 500 ended up giving its worst first half performance of any year since 1970.

- European equities struggled the most in June. The EU levied additional sanctions on Russian oil at the beginning of the month which once again caused headwinds as the region is trying to resolve the issue of replacing the big hole left by Russian commodities imports. The UK market also struggled as it announced the highest inflation print it has received within four decades.

- The types of inflationary pressures have shifted through the period with the initial surge in US inflation driven by durable goods. However, the most recent surge of inflation is due to services, and European inflation is being led by the energy sector.

- Central banks have continued their battle against inflation:

- The Fed continued to tighten financial conditions and raised the fund’s rate by 75bp – the largest increase in over 27 years. Following concerns of higher inflation, the Fed stated they are still committed to combating inflation and making it a priority.

- The ECB continued their path and announced the end of net asset purchases under APP beginning in July. They also showed their intention to raise interest rates at meetings in July and September.

- In the UK, the Bank of England delivered another rate hike of 25bps while continuing to imply its readiness to adjust its pace in response to changes to the economic outlook. UK inflation also hit a four-decade high of 9.1%.

- The 10-Year US treasury had a tale of two halves story in June with the beginning of the month showing the continued trend of increasing yields and the last half of the month showed yields falling. Early on in the month, the US 10-Year Treasury yield rose 20 bps alone in response to the ECB’s policy, a greater-than-expected US inflation print and central bank plans for more aggressive monetary policies. In the second half of June, global sovereign yields started falling in response to concerns surrounding economic growth and recessions.

- In Europe, the European Central Bank’s (ECB) indication of potential rate hikes at upcoming meetings increased yields in the first half of June. Towards the end of the month at the ECB annual summit, central banks put forward a united front.

- It’s becoming increasingly clear that central banks are facing a growth-inflation trade-off, in which they are siding with inflation. The issue and concerns are that hiking interest rates too often will increase the risks of a recession, while not tightening enough risks causing unanchored inflation expectations. Many central banks like the Fed and BoE have made clear it is ready to dampen growth.

How did Factors Perform in June?

While equities around the world have continued to struggle YTD, the Minimum Volatility index has shown to offer protection from the full downside blow of the drawdown. The equity market has seen continued volatility coming from geopolitical, inflation, and tighter monetary policy concerns. Nevertheless, the Minimum Volatility Index has been the best-performing factor in June, the past 3-months and the second best-performing factor YTD.

Blog Post by Raj Chana

Investment Analyst at ebi Portfolios.

What else have we been talking about?

- Q2 Market Review 2024

- June Market Review 2024

- Do Political Events Impact Financial Markets?

- Is there an AI bubble?

- May Market Review 2024