Overall Market Backdrop for Q2

- Q2 proved a continuation of Q1 for global equities as they once again had a disappointing run as familiar headwinds of growth concerns, inflation and volatility played puppet master.

- While Emerging markets do not have the same issues as the developed world, the result is still similar with the region struggling in Q2.

- Increasing inflation prints globally have once again put downward pressure on bonds in Q2. Towards the end of the month, central banks continued to announce hawkish policies to combat inflation and we saw yields begin to drop from a peak of 3.48% to the final figure of 2.97% (US 10-Year Treasury).

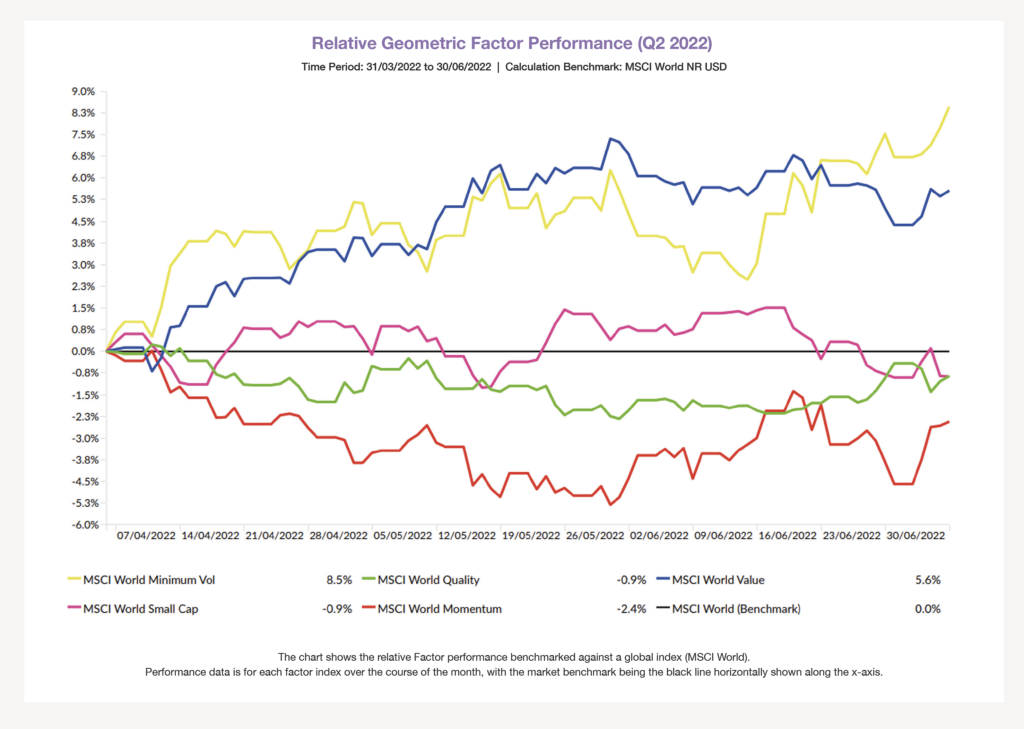

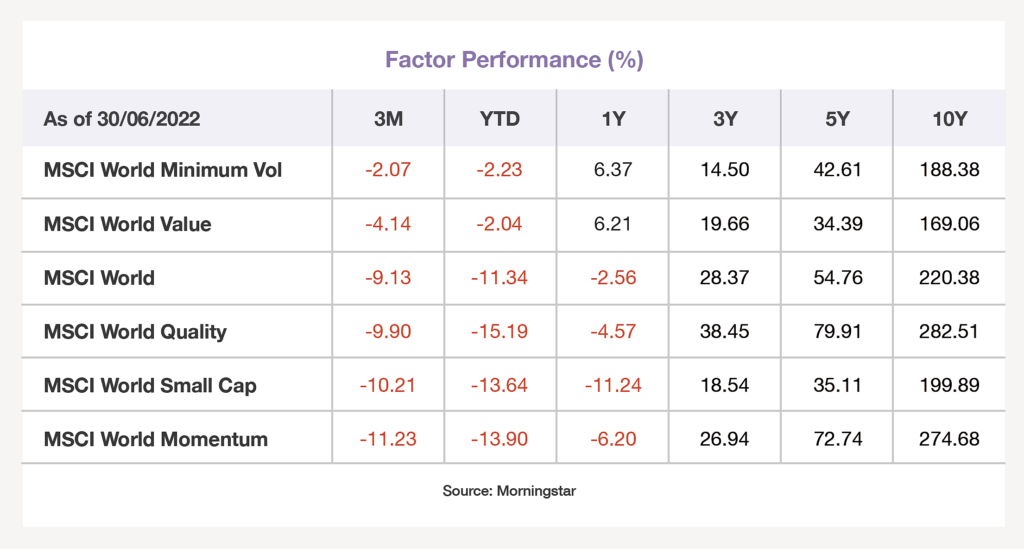

- Minimum Volatility has been the best performing factor for Q2.

Drivers of Market Conditions in Q2

- The tough start that equities had in Q1 2022 got a lot tougher in Q2. Headwinds proved too hot to handle and this is now the worst first half of the year for developed market equities in over 50 years. Global equities have had a poor run and investor sentiment in developed countries are at low levels. Global equities not only have had to deal with rising inflation and slowing growth rates but also the unfortunate combination of the continuing war in Ukraine and lockdowns in China hampering global supply chains again. The other concern for the US comes from the potential side effects of the Fed getting inflation under control. The Fed had forecasted that unemployment will need to rise to just above 4% to get inflation to manageable levels but there are concerns that unemployment may need to rise much higher.

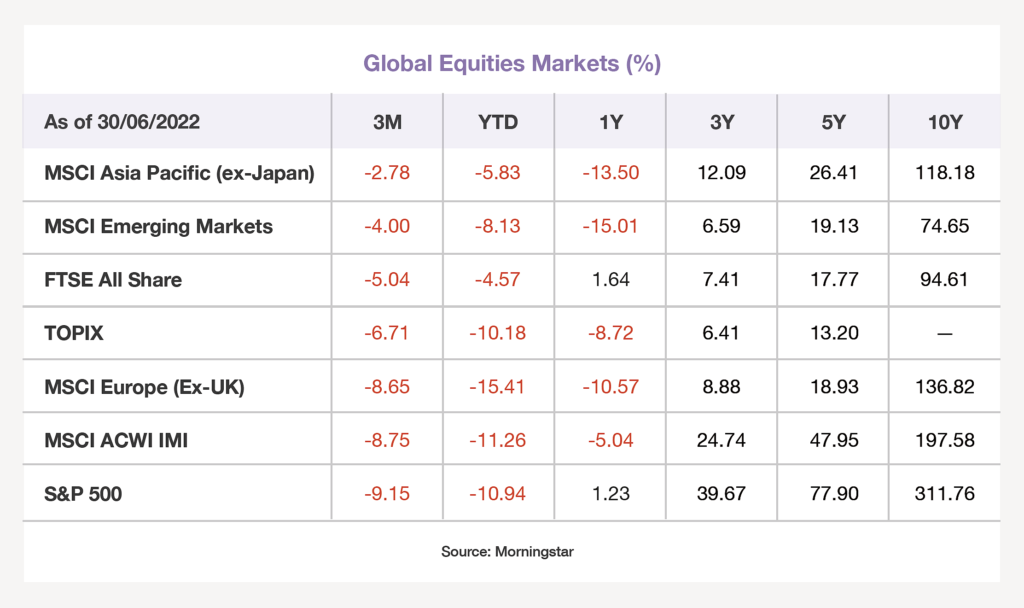

- At the start of the quarter US equities were overwhelmed with inflation standing at 8.5%, the highest level since 1981. As a result, the Federal Reserve (Fed) continued on its hawkish sentiment which hurt growth style equities, with the technology industry being the hardest hit. US equities also had to deal with a battle on another front early on in Q2 as China set in place regional lockdowns which once again damaged supply chains around the world. Investor sentiment went from bad to worse throughout the quarter with the same usual suspect of surging inflation being the epicentre of fear. Equity market volatility was common in every region in Q2, with the VIX index increasing by approximately 40% by the end of the quarter. The amalgamation of bad segments of the US earnings reports, weakening consumer demand, central bank tightening, rising and persistent inflation, higher sovereign yields and slowing economic growth made the S&P 500 the worse-performing equity index for Q2 2022.

- While European and UK equities performed better than US equities, they still saw negative returns for the quarter. The reoccurring themes among all equity regions are fears surrounding growth rates, high inflation and tighter financial conditions. However, European equities have been more affected by the geopolitical conflict in Ukraine and with no signs of a resolution yet the European economy continues to suffer. With the EU continuing to increase sanctions on Russian commodities it’s also damaging its own supply chains and the race to find alternative supplies has started.

- The Bank of England (BoE) offered a statement that they are now entering a period of high recessionary risk, and with the UK and the rest of Europe feeling the effects of high inflation spearheaded by spiralling food and energy prices, investor sentiment has been damaged and has fallen to record lows. Even with the UK announcing a stimulus package to try and tackle the country’s cost of living crisis, it proved to provide no respite as the region continued to struggle and announced the highest inflation print it has received within four decades. The UK economy is also having to deal with the cost of living and consumers are feeling the squeeze from negative real wage growth. The combination of rising mortgage rates and higher food and energy prices is dealing a blow to consumers around the UK.

- Now, let’s address the elephant in the room, Inflation. Inflation has caused the biggest headwind to global equities this year. However, the surges of inflation have shifted, initially, we saw the surge in US inflation driven by durable goods but now we have seen this transition into services. In Europe, we have seen inflation being driven by the energy sector. With this being said, the two biggest contributors in terms of sectors have been the energy and housing sectors. House prices are now at record highs and in the US and UK, mortgage rates have increased rapidly YTD.

- Central banks continue to work on a tightrope to try and balance the ongoing high inflation with a slowing growth rate. It is now becoming increasingly clear that the growth-inflation trade-off that central banks have is beginning to fade as the priority is becoming inflation. The issue and concerns are that hiking interest rates too often will increase the risks of a recession, while not tightening enough risks causing unanchored inflation expectations. Many central banks like the Fed and BoE have made clear it is ready to dampen growth:

- The Fed continued to tighten financial conditions and raised the fund’s rate by 75bp – the largest increase in over 27 years. Following concerns of higher inflation, the Fed stated they are still committed to combating inflation and making it a priority.

- The ECB continued their path and announced the end of net asset purchases under APP beginning in July. They also showed their intention to raise interest rates at meetings in July and September.

- In the UK, the Bank of England delivered another rate hike of 25bps while continuing to imply its readiness to adjust its pace in response to changes to the economic outlook. UK inflation also hit a four-decade high of 9.1%.

- International Bond yields continued to rise throughout the best part of the quarter and the US 10-year ended at 2.97% which is a 28% increase from the starting yield. At the start of Q2, the increased likelihood of more of an aggressive monetary policy stance increased yields. Although yields did increase overall we did see some fightback and this was mainly due to increased concerns over an economic slowdown, persistent inflation and the Covid-19 breakout in China. During the course of the quarter, we saw economic data such as greater-than-expected inflation prints continue to push yields higher. However, towards the late stages of Q2, global sovereign yields started falling in response to concerns surrounding economic growth and recessions, with the continued sell-off of growth-style equities also pushing investors towards bonds as they searched for safety amid the chaos.

- While Emerging Markets and the Asia Pacific (ex-Japan) market did not have positive performance in the quarter, they did do notably better than developed equities. The Chinese market has great influence over both equity indexes. At the start of Q2, the Chinese government struggled to contain major outbreaks of covid and Shanghai endured some of the severest lockdown rules which have damaged market sentiment and supply chains. Throughout the quarter, reopening occurred alongside positive sentiment coming from Chinese export data crushing expectations. June proved to be a great month for Chinese equities with the manufacturing sector springing back to life resulting in the second-steepest monthly expansion of output seen for over a decade. The Asia Pacific (ex-Japan) index also benefits greatly from only having 1.35% of its weighting in the technology sector.

How did Factors Perform in Q2?

- While not having a positive return, the Minimum Volatility factor has performed better than the market and shielded itself from the full brunt of the economic environment, just as it did in Q1, and is now the best performing factor for the Quarter and second-best so far in 2022. Q2 offered the same trials and tribulations as Q1 with the headline being high inflation and high volatility. The combination of continued volatility coming from geopolitical, inflation and growth worries and weakened investors has created the optimal environment for the Minimum Volatility factor. The factor deliberately seeks to curtail upside moves by enhancing support on the downside, and we can see this in Q2 as the factor did precisely what it is engineered to do and acted as a safeguard against periods of uncertainty and volatility.

- Throughout the year Momentum has struggled due to its saturation into IT stocks stemming from a stellar performance in 2021. For this reason, momentum funds have been hit extremely hard by the hawkish sentiment coming from central banks (in particular the Fed) which has hurt growth-style equities (the MSCI Information Technology index has returned -15.08% in Q2). With the stellar performance of the Energy sector YTD (28.89%) data is now showing a huge shift in the sector exposure for the momentum index as of 30/06/2022, with the index now having an underweight in the technology sector and an overweight in the energy sector.

[1] Hawkish – When you call a statement or policy hawkish it tends to mean that the policymaker is choosing to use high-interest rates to curb inflation. Hawkish policies tend to generally ignore economic growth impacts but, support an economy operating at a level below its full-employment equilibrium.

[2] APP (Asset purchase programmes) – The ECB’s asset purchase programme is part of a package of non-standard monetary policy measures that helps the ECB keep inflation below but close to 2%. This also includes targeted longer-term refinancing operations, which were initiated in mid-2014 to support the monetary policy transmission mechanism and provide the amount of policy accommodation needed to ensure price stability.

Blog Post by Raj Chana

Investment Analyst at ebi Portfolios.

What else have we been talking about?

- Q2 Market Review 2024

- June Market Review 2024

- Do Political Events Impact Financial Markets?

- Is there an AI bubble?

- May Market Review 2024