December Economic Background

• Central banks take a cautious step towards easing as growth momentum cools

• AI enthusiasm continues to drive markets, but valuation concerns refuse to fade

• Rare earth tensions between the US and China ease temporarily, but strategic risks remain

Source: Morningstar (Morningstar Global Markets; Bloomberg Global Aggregate)

Market Review

Central banks begin to ease interest rates

December marked an important turning point for global monetary policy, as major central banks signalled that the fight against inflation is largely behind them and attention is gradually shifting towards supporting slowing economies. However, the pace and confidence of this transition varied meaningfully across regions.

In the US, the Federal Reserve (the Fed) cut interest rates by 0.25% on 10th December, pointing to continued disinflation and a cooling labour market. While economic growth has remained reasonably resilient, policymakers judged that interest rates no longer needed to remain as restrictive. Fed Chair Jerome Powell reiterated that any further cuts would be cautious and data-dependent, particularly given the disruption to economic data following October’s government shutdown. The decision proved more divisive than recent meetings, with three members dissenting (the highest number since 2019) highlighting internal disagreement over whether the economy requires further support or risks overheating again if easing goes too far.

In the UK, the Bank of England (BoE) also reduced interest rates by 0.25%, from 4% to 3.75%. Falling consumer price inflation and increasing signs of spare capacity in the economy provided the justification, but the decision was finely balanced, passing by a narrow 5-4 vote. Policymakers remain concerned that inflation pressures, particularly in services, have not fully disappeared. As a result, the BoE stressed that further cuts are not automatic and will depend on continued progress.

By contrast, the European Central Bank (ECB) opted to keep rates unchanged at its 18th December meeting. With consumer price inflation close to target and early signs that growth is stabilising, the ECB chose to pause after earlier easing, maintaining its “meeting-by-meeting” approach and avoiding any firm guidance on future moves.

Taken together, December’s decisions underline a clear shift away from aggressive inflation-fighting and towards carefully nurturing growth, while remaining alert to the risk of inflation re-emerging.

AI optimism drives markets, but caution builds

Equity markets continued to be dominated by artificial intelligence (AI) themes in December, as excitement around productivity gains and long-term growth opportunities remained strong. US indices, including the S&P 500 and Nasdaq, reached record highs, led once again by mega-cap technology and AI-focused stocks. However, beneath the surface, investor sentiment was increasingly volatile. Rising valuations, heavy market concentration in a small group of technology giants, and growing levels of corporate debt linked to AI infrastructure spending have kept concerns about a potential AI-driven bubble firmly in focus.

The cloud services provider Oracle offered a timely example of this tension. Despite announcing increased investment in AI capabilities, weaker-than-expected revenue guidance triggered a sharp fall in its share price. The reaction highlighted how sensitive markets have become to execution risk and the ability of companies to convert AI spending into sustainable profits.

Debate continues over whether the current surge in AI investment reflects justified long-term growth or speculative excess. Investors and regulators alike are watching closely as spending accelerates on data centres, cloud infrastructure, and AI deployment, alongside increasing scrutiny of regulation and energy usage. For investors, the key message remains familiar: AI is likely to be a powerful long-term driver of growth, but valuations matter. Maintaining diversification and avoiding over-reliance on a narrow set of stocks remains crucial in navigating this phase of the market.

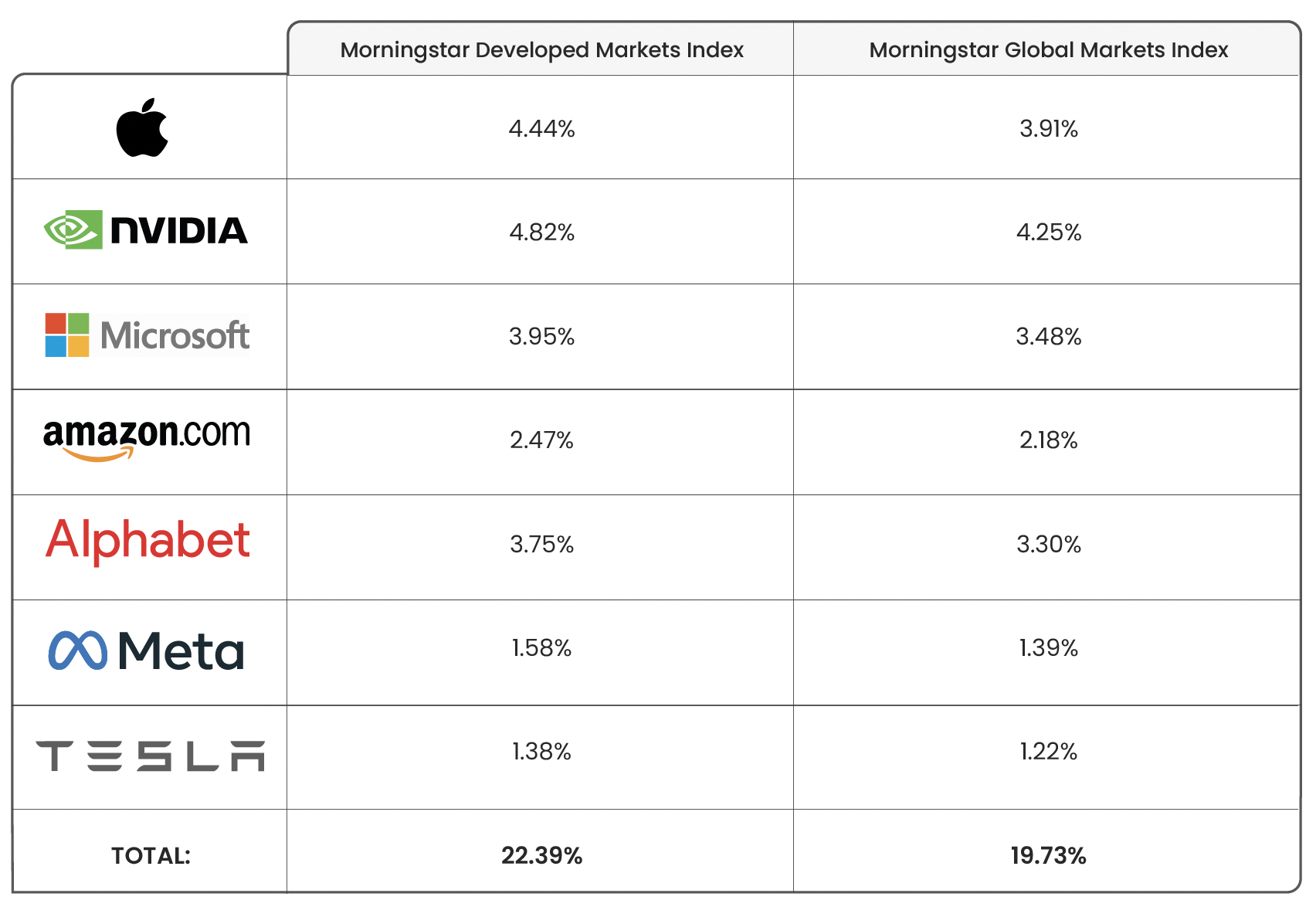

“Magnificent Seven” Concentration

(weighting % as of 31.12.2025)

Source: Morningstar. Data as of 31.12.2025.

Morningstar Developed Markets Index: measures the performance of large-, mid- and small-cap stocks in developed markets around the world, representing the top 97% of the investable universe by market capitalisation.

Morningstar Global Markets Index: measures the performance of large-, mid- and small-cap stocks in developed and emerging markets around the world, representing the top 97% of the investable universe by market capitalisation.

Rare Earth tensions ease, but the US-China strategic battle continues

Rare earth elements, essential to industries ranging from electric vehicles and renewable energy to defence and advanced technology, remained a central feature of US-China relations in December. China continues to dominate global rare earth supply chains, giving it significant economic and geopolitical leverage, a position likely to grow more important as the clean-energy transition accelerates.

Following earlier export curbs and tighter licensing requirements, a recent easing of tensions has led to more streamlined export approvals for selected customers, including suppliers linked to US automakers. This “trade truce” has helped alleviate short-term supply concerns and signals a willingness from both sides to stabilise relations, at least temporarily. However, China’s underlying control of critical materials remains firmly intact. In response, the US has combined diplomatic engagement with a longer-term strategic push to reduce dependence on Chinese supply. This includes accelerating domestic rare earth production, offering investment incentives, and strengthening partnerships with allied nations to build more resilient supply chains.

While immediate pressures have eased, policymakers on both sides have made it clear that rare earths remain a strategic priority rather than a resolved issue. As a result, these critical materials look set to continue playing a key role in US-China relations well into 2026 and beyond.

For financial professionals only.

Disclaimer

We do not accept any liability for any loss or damage which is incurred from you acting or not acting as a result of reading any of our publications. You acknowledge that you use the information we provide at your own risk.

Our publications do not offer investment advice and nothing in them should be construed as investment advice. Our publications provide information and education for financial advisers who have the relevant expertise to make investment decisions without advice and is not intended for individual investors.

The information we publish has been obtained from or is based on sources that we believe to be accurate and complete. Where the information consists of pricing or performance data, the data contained therein has been obtained from company reports, financial reporting services, periodicals, and other sources believed reliable. Although reasonable care has been taken, we cannot guarantee the accuracy or completeness of any information we publish. Any opinions that we publish may be wrong and may change at any time. You should always carry out your own independent verification of facts and data before making any investment decisions.

The price of shares and investments and the income derived from them can go down as well as up, and investors may not get back the amount they invested.

Past performance is not necessarily a guide to future performance.

Blog Post by Jonathan Simpson

Investment Oversight Analyst at ebi Portfolios

What else have we been talking about?

- April Market Review 2026

- Q1 Market Review 2026

- March Market Review 2026

- Middle East conflict

- February Market Review 2026