Comparing ESG Scores

Spring 2020 was a landmark quarter for Environmental, Social and Governance (ESG) fund sales with 76% of European fund inflows allocated to ESG tilted choices. This is way ahead of the US experience suggesting a divergence of investor preferences, with Europe leading the ESG charge.

Yet securing analytical evidence for outperformance between funds claiming an ESG characteristic is more of a nuanced story. There are some studies showing outperformance whilst others show the opposite. With claims of ESG compliance mushrooming, it is worth probing the strength of the link between ESG performance, typically measured using scoring systems, and the equity performance.

Over recent decades, there have been more than 2,000 empirical studies and several review studies on the relation between various ESG criteria and stock performance. Many studies document outperformance of ESG funds (1) or at least that you can “do equally well or badly while doing good” (2) using a variety of metrics such as the MSCI ESG STATS data.

Within the ESG sphere many investors have a different focus of interest. A few of the studies focus solely on one ESG element, such as governance, and develop tailored metrics better suited to different geographies. For example, with governance it might be considered important to identify variations across countries which exist for a variety of reasons such as different ownership structures, varied shareholder priorities and variation between the broad institutional and legal settings.

Each ESG ratings provider, such as MSCI and Sustainalytics, have developed different sub-scoring systems to support their summary scores. They make judgements to weight these sub-scores to arrive at overall scores. This is a recipe for some very different cocktails within ESG scores.

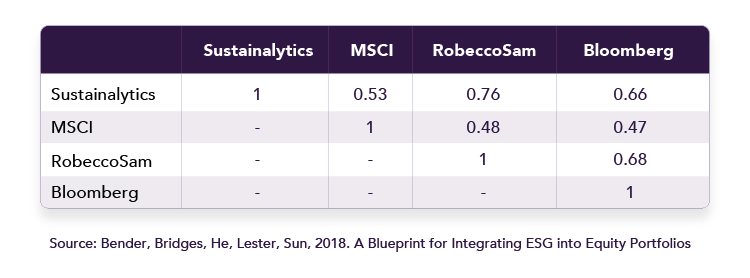

ESG studies are typically based on different metrics or scoring systems to define what ESG represents and scoring systems can generate markedly different results for the same funds. For example recent research suggests scoring systems from MSCI, Sustainalytics and other providers are far from standardized, as shown in this table ranking correlation of the different scoring systems from 0 to 1.

ESG Scores: Correlated But Different

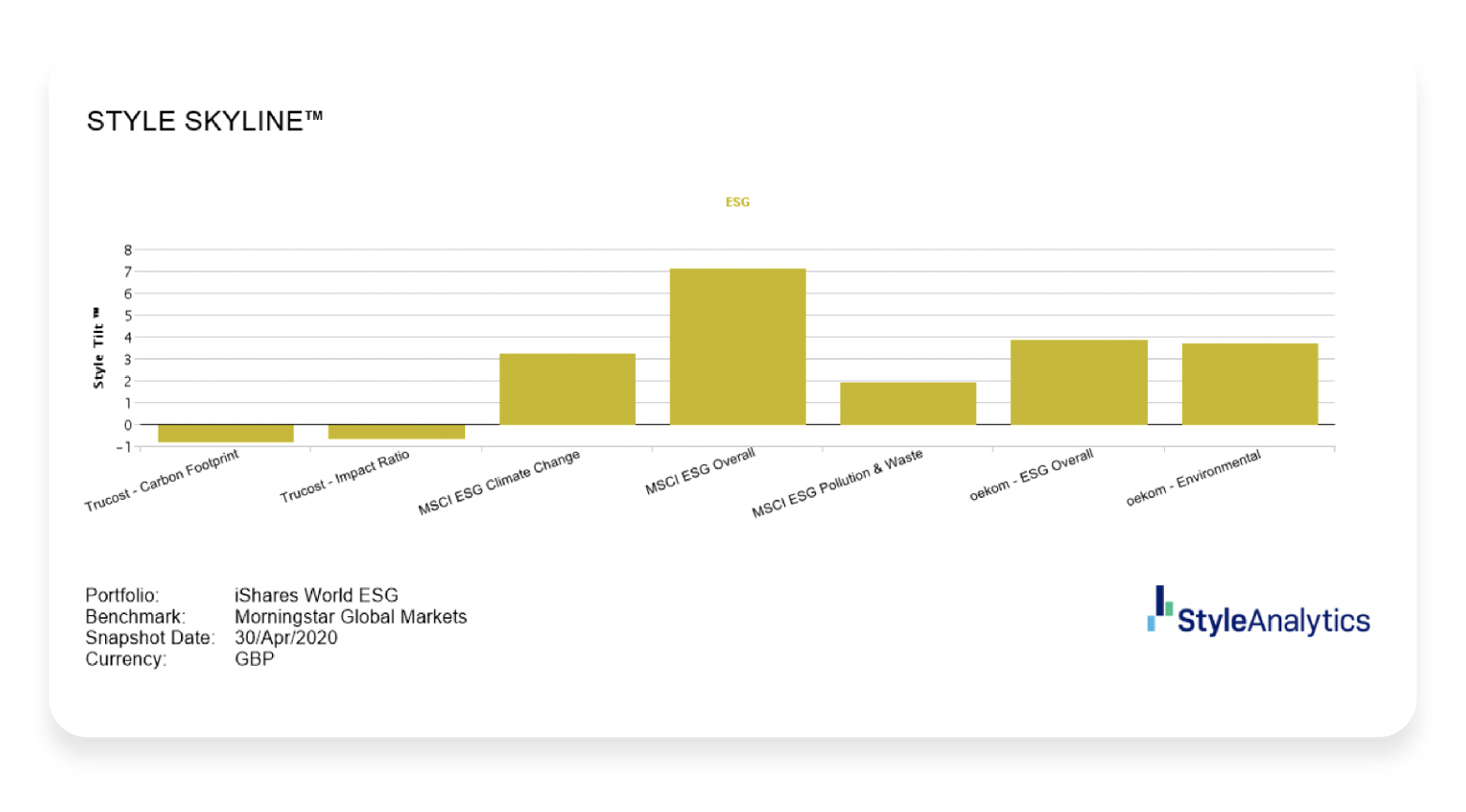

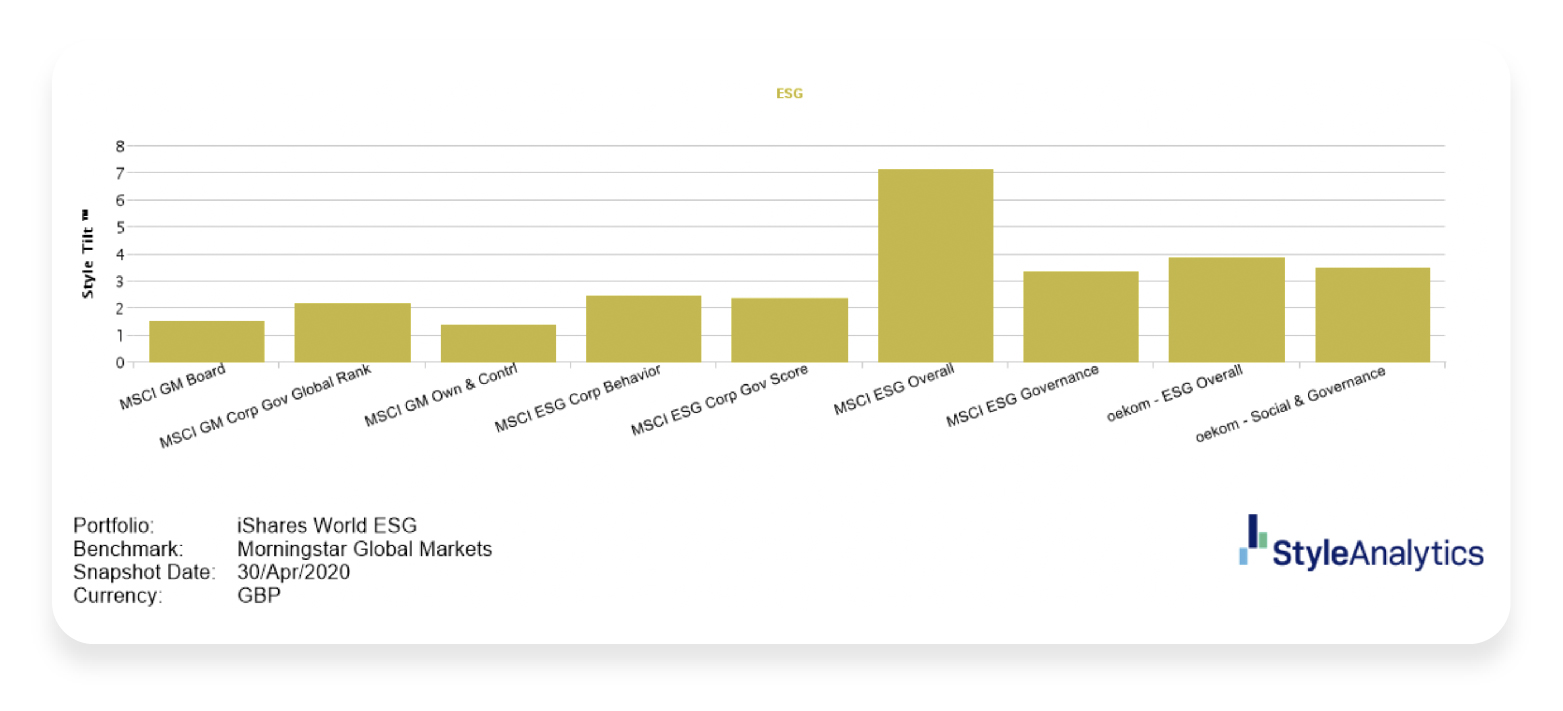

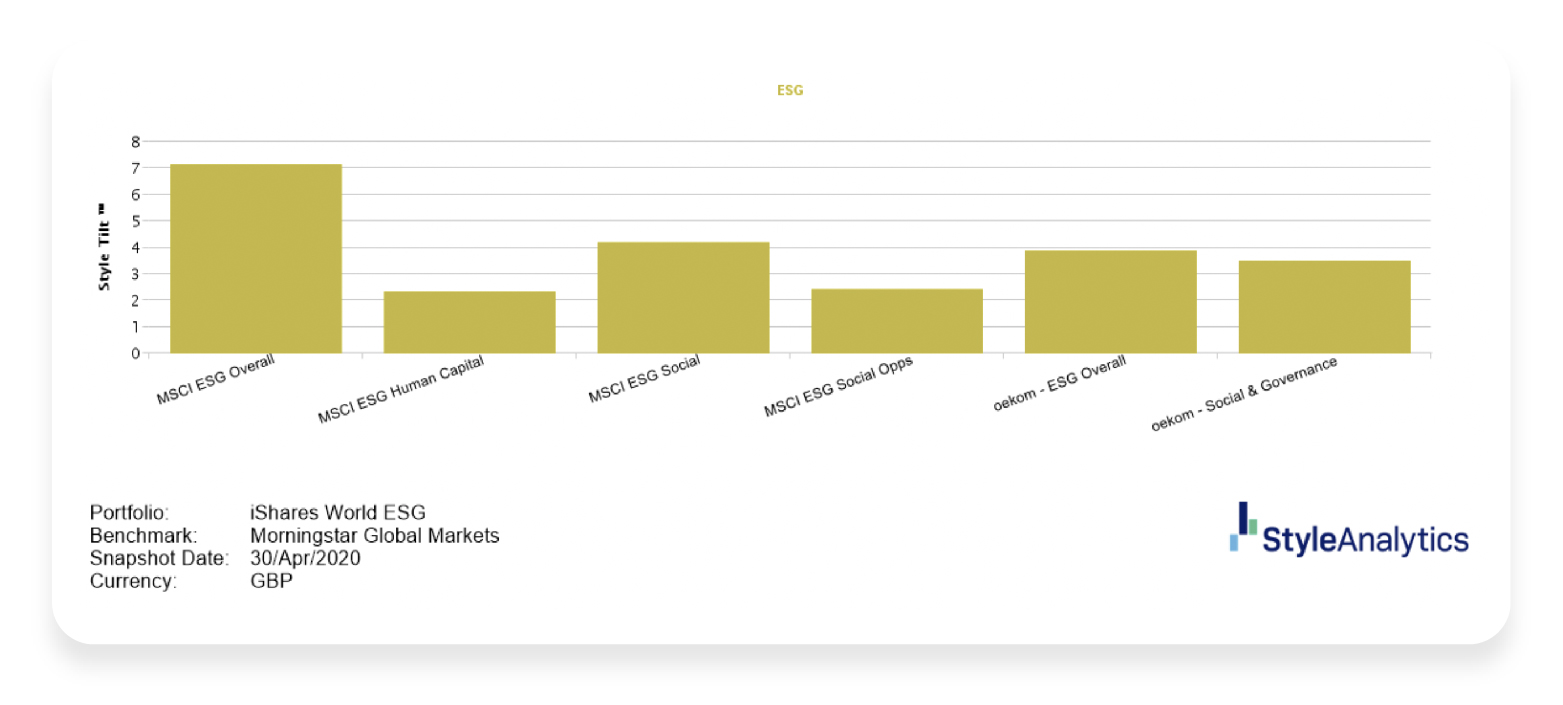

We can use Style Analytics, a provider of style and factor risk information, to identify and decompose the style tilts for a fund such as the ishares World ESG Fund. The scale on the left of each of the next three bar charts is an indication of the strength of the ESG signal (or t-statistic for the maths fans amongst us).

Starting our analysis of the ishares World ESG Fund in order to decompose the Environmental dimensions, we can see that the Trucost – Carbon Footprint score, compiled from reported data assessing greenhouse gas emissions of 4,500 companies worldwide, is essentially bang on the benchmark with no tilt either way. In contrast the Oekom indices are suggesting a clear tilt in this ESG Fund away from the benchmark although not as strong a tilt as is suggested by the MSCI ESG Overall score. A sub-score, the MSCI ESG Pollution & Waste score, is a relatively weaker tilt although still statistically significant.

Turning to Governance, weak signals for this Fund show up in two of the scoring systems. MSCI Governance Metrics – Board, one of four corporate governance themes ranked by MSCI, is showing up as relatively similar to the benchmark. Similarly, another scoring system, the MSCI Governance Metrics – Ownership and Control, is not showing statistical significance compared to the benchmark.

In contrast sub-scores for oekom -Social & Governance, MSCI ESG Governance and MSCI ESG Governance are strongly significant compared to the benchmark. Whilst both the composite scoring systems, MSCI ESG Overall and oekom – ESG Overall, are strongly statistically significant suggesting explanatory power.

Finally, with the social dimension of ESG we see strong statistical significance across the board of scoring systems. This ranges across all social metrics including the MSCI ESG Social, oekom – ESG Social and MSCI ESG Human Capital sub-scores, suggesting the Fund is doing its job in this area.

For the ishares World ESG Fund under analysis, factual metrics including greenhouse gas emissions (GHGs) are weaker signals, offering less discrimination from the benchmark than more subjective dimensions such as those falling under the MSCI’s social pillar which covers human capital, product liability, stakeholder opposition and social opportunities. Where elements of subjectivity intrude then the metrics diverge further from the benchmark even for an index fund with an ESG tilt.

An understanding of the different ways ESG metrics behave is essential for investors to see past dubious claims of ESG compliance and meet their ESG goals as well as ensure that performance after costs and fees is acceptable.

Investors more focused on corporate governance may choose to prefer MSCI’s ESG measures. A carbon-focused investor may prefer Trucost metrics, whilst an investor focused on the social aspects may prefer to rely on oekom. Some composite or combination of these might suit other investor preferences.

Alongside the potential subjectivity and transparency around ESG scores, there are all the usual pitfalls to consider in assessing ESG funds, not least survivorship bias, the tendency of only outperforming funds to survive. Some ESG funds do have a tendency to be overweighted in tech companies, which can be more volatile in the short term. Others avoid the smaller companies, often in traditional sectors and dirty industries. ‘Greenwashing’, or making your fund sound more green and ESG-compliant than it is, has long been a scourge of the ESG sector. An option to minimize such pitfalls is to outsource ESG investments to a portfolio provider with a reputation for thorough research.

(1) Kempf and Osthoff, 2007; Derwall, Koedijk, and Ter Horst 2011