David Rosenberg @EconguyRosie:

“One silver lining from the stock market’s horrible behaviour is that we haven’t had a presidential tweet since Oct 31st”. (Gluskin Sheff Chief Economist).

The Fed Funds Futures contract for December was, (as of Tuesday), pricing in a c.64% chance of the Fed raising interest rates at their next meeting (December 18th/19th), well below what pertained just a few short weeks ago, when it was a more or less done deal, (82%), with three more rate hikes penciled in for 2019. On October 3rd, Jerome Powell, the Federal Reserve Chairman opined that the “Neutral” Fed Funds rate [1], stating that the Fed Funds rate was “a long way from Neutral”. On the 28th November, he said that it is “just below the broad range of estimates of the level that would be neutral for the economy.” That damascene conversion occurred despite few data points over the period that suggested that economic conditions have meaningfully changed – except one (or more precisely, three).

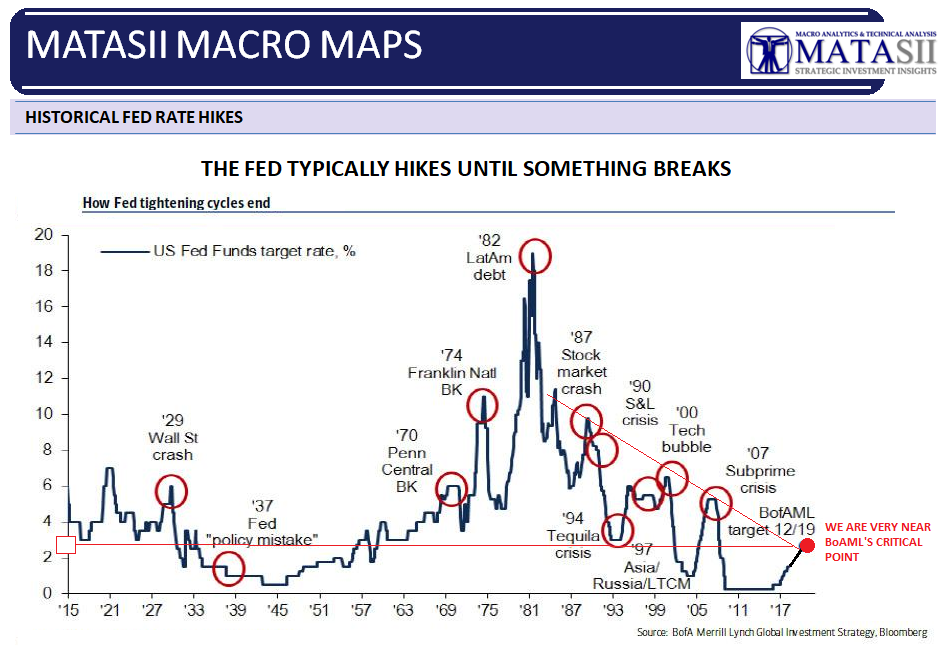

Why this relatively drastic re-assessment of the state of the economy has occurred is hard to fathom. It may be that Donald Trump’s relentless pressure on the Fed has taken its toll, (he is a “low-interest rates guy” after all); it may be that the original comments were the catalyst for a sharp rise in 2 year bond yields, which in turn tightened financial conditions (High Yield spreads rose over 1% post the October announcement), sufficiently to “break” something, (the markets, or the economy). The Fed has “previous” in this regard as the chart below demonstrates. This has manifested itself in yield curve inversions [2], which are widely believed to be the harbinger of recession.

{kind=link}

{kind=link}

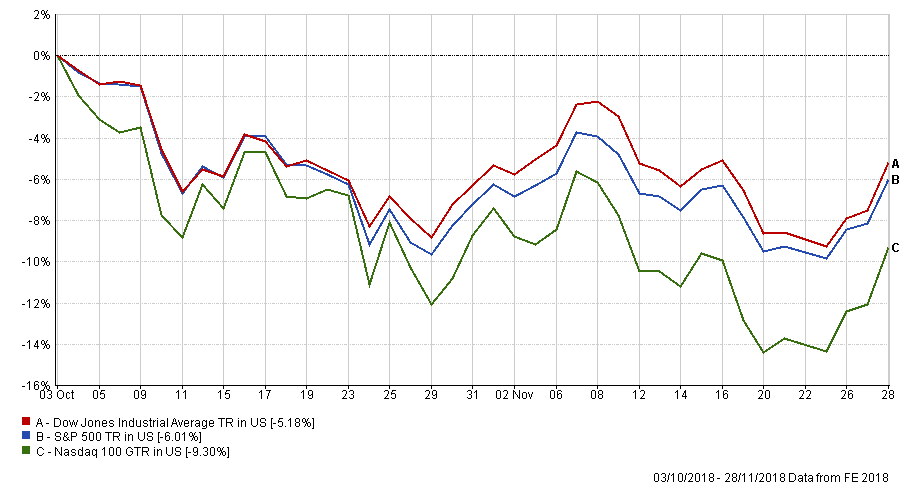

After nearly two decades of Greenspan, Bernanke and Yellen, markets had become accustomed to low (and ever lower) interest rates and so were understandably skeptical that he would raise rates, but Powell did so, despite the protests of Trump. He (Powell) gave the impression that he was not overly concerned by stock price falls and has expressed concerns about whether (or if at all) market intervention should be considered due to the moral hazard implications thereof. The abrupt volte-face suggests that his tolerance for market declines (c.10% seems to be enough), is not measurably different from his predecessors – the Powell Put has been born and at a level a fair bit higher than previously imagined. Markets reacted extremely positively, though it hasn’t lasted for long, as other worries have again taken precedence (China in particular).

Until last month it appeared that the Fed was on auto-pilot, raising rates to try to get up to a reasonable level (partly to give them some “ammunition” to deal with the next economic downturn); now it appears they are once again “data dependent”, by which they mean markets to infer that stronger data will mean more rate hikes (and vice versa). The problem is in determining which data the Fed is looking at – it appears that the most important data can be found here. If they ARE looking for reasons to halt rate rises, this (or this), may be better ones. They indicate both that inflation exectations are falling and that financial conditions are tightening.

{kind=link}

{kind=link}

Markets are unsettled. Torn the impulse to buy aggressively every time the Fed seems to be relenting on rate rises, investors are clearly becoming acutely aware of the second order issues raised by the pause – what does it say about the outlook for both equities if growth is slowing and what are the implications for Corporate bonds, given that US Corporate debt is at record levels? Investors appear paralysed with indecision, which might explain the wild gyrations of recent weeks. It is starting to look as if our past comments on whether the Global Economy can cope with the higher rates (spoiler alert- it can’t), that the Fed wishes to see is germane here – the question then becomes, will the Central Bank(s) react quickly enough in the face of a slowdown, or like in 2000 and again in 2007 will they all be left behind, as the markets go into full “risk off” mode? For now, this is a worrry for the future.

{kind=link}

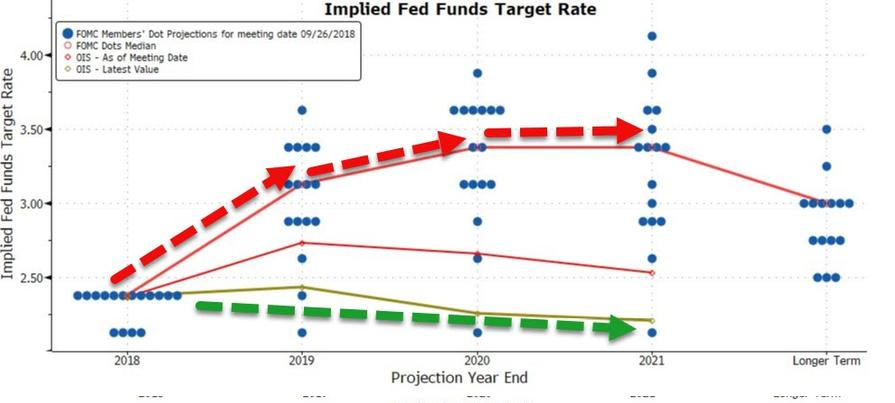

In the event, the Fed DID raise rates by another 0.25%, leading to another sharp sell-off; they did cut their estimate of the number of rate hikes needed in 2019 (from three to two). But as the chart below shows, there is still a chasm between Fed and market expectations for the future path of interest rates [3]. Markets are now projecting NO further rate rises for the next two years.

In the last 2 days, there has been a crescendo of pundits and market analysts proclaiming that the Fed has made a policy error [4] and that recession was around the corner but is the market right? Of course, the Fed cannot directly endorse the current bearishness (no Central Bank could do so without admitting that they had failed in their mandate to facilitate growth), but there is a large element of vested interest in the views of market participants. Used to being able to dictate policy under Bernanke and Yellen, (a market decline has led to abrupt back-tracks in stated rate rise intentions), the market appears to be having another “tantrum”, to try to force the maintenance of low-interest rates in perpetuity. The US economy, however, is doing well at the moment, with unemployment around 50-year lows and wages starting to rise, but of course, the bull market has been predicated on the opposite (bad economic news = lower interest rates = share price gains). It used to be said that what was good for Wall Street was good for Main Street, but this appears to no longer be the case; the former has had an extended party for the last decade, whilst the real economy suffered, but this may be about to reverse (and of course Wall Street is not happy). The polarisation in the US polity is being mirrored in the divide between financial markets and the rest of the economy, but as to the future path of interest rates, either the Fed or the markets are going to be very wrong, very soon.

As for Mr President, he may have to get used to this schizophrenia. What is somewhat perplexing though is why he hitched his wagon to the stock market in the first place; latest data suggests that ownership of stocks is heavily skewed towards the wealthy, who are not his natural supporters, which begs the question of why he sees it as so important to cheerlead markets higher. Still, if this is the only thing about which Trump confuses you, you’re doing pretty well…

[1] The Neutral rate would be the level at which Interest Rates were neither stimulatory for the economy nor restrictive; how anyone knows what this level actually is is beyond me, but I digress.

[2] A yield curve inversion occurs when short-dated bonds yield more than longer-dated versions. One would normally expect to receive a premium (a maturity premium) for investing in longer-dated bonds; when this is not the case, it implies that growth is predicted to fall. Investors thus buy the latter to “lock in” those yields for a longer period of time. The shorter-dated bonds are much more heavily influenced by Fed policy (and thus won’t start to rise in price/fall in yield significantly until the Fed actually cuts rates).

[3] The “Dot Plots” show the expectations of the 12 board members of the Federal Reserve for where the Fed Funds rate will be at a specific point in time. This article gives a good primer on what it is (and isn’t).

[4] Some might argue that the real “error” was in leaving interest rates far too low for far too long, allowing a speculative bubble to develop which Messers Greenspan, Bernanke, and Yellen continually refused to acknowledge, let alone deal with. Jerome Powell has not spent his career in academia and is thus much more acquainted with the real world.

Disclaimer

We do not accept any liability for any loss or damage which is incurred from you acting or not acting as a result of reading any of our publications. You acknowledge that you use the information we provide at your own risk.

Our publications do not offer investment advice and nothing in them should be construed as investment advice. Our publications provide information and education for financial advisers who have the relevant expertise to make investment decisions without advice and is not intended for individual investors.

The information we publish has been obtained from or is based on sources that we believe to be accurate and complete. Where the information consists of pricing or performance data, the data contained therein has been obtained from company reports, financial reporting services, periodicals, and other sources believed reliable. Although reasonable care has been taken, we cannot guarantee the accuracy or completeness of any information we publish. Any opinions that we publish may be wrong and may change at any time. You should always carry out your own independent verification of facts and data before making any investment decisions.

The price of shares and investments and the income derived from them can go down as well as up, and investors may not get back the amount they invested.

Past performance is not necessarily a guide to future performance.