March Economic Background

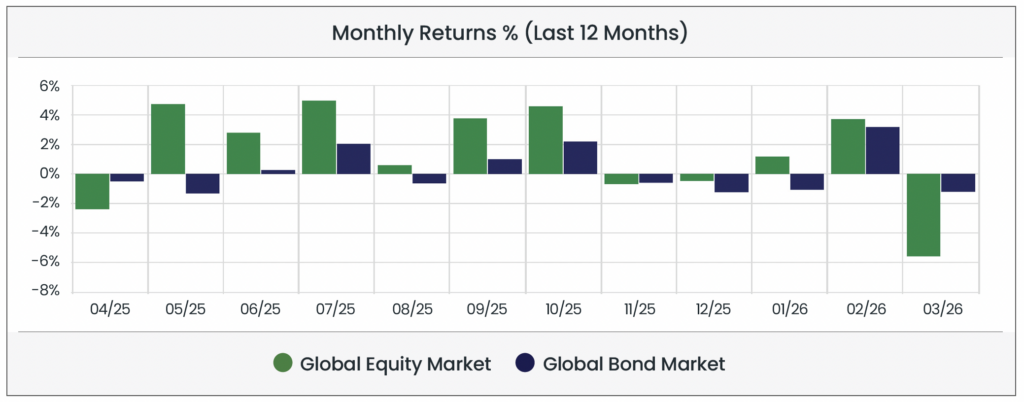

March was largely defined by a single, seismic event: the outbreak of direct military conflict between the United States/Israel and Iran. Following US and Israeli air strikes on Iran on 28th February, markets were engulfed in the most severe geopolitical and energy shock in years. Oil prices surged by as much as 50% in the space of weeks, global bonds sold off as investors reappraised the inflation outlook, and equities fell across the board. Global equities returned -5.58% for the month, while global bonds returned -1.18%. The conflict rapidly spread beyond Iran’s borders, disrupting shipping through the Strait of Hormuz, one of the world’s most critical energy chokepoints, triggering a sweeping reassessment of the global economic and interest rate outlook.

Equity & Bond Performance (Last 3 Months)

Source: Morningstar (Morningstar Global Markets; Bloomberg Global Agg). Data as of 31/03/2026 in GBP terms.

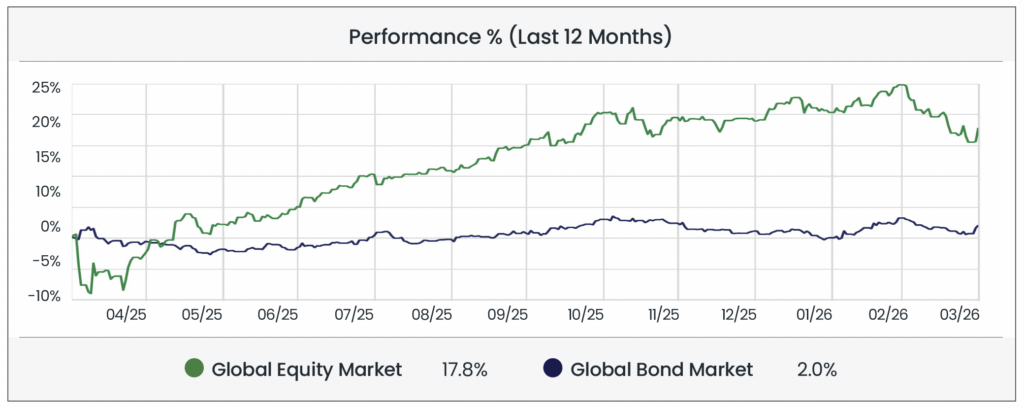

Source: Morningstar (Morningstar Global Markets; Bloomberg Global Agg). Data as of 31/03/2026 in GBP terms.

Source: Morningstar (Morningstar Global Markets; Bloomberg Global Agg). Data as of 31/03/2026 in GBP terms.

Economic Background

War in the Middle East dominates global markets

The month began with a dramatic escalation in geopolitical risk. On the night of 28th February, US and Israeli forces launched air strikes on Iran, killing Supreme Leader Ayatollah Ali Khamenei and senior military commanders including the head of the Revolutionary Guard. Iran responded swiftly with waves of missiles and drones targeted at Israel and US allies across the Gulf, plunging the region into its widest war in decades.

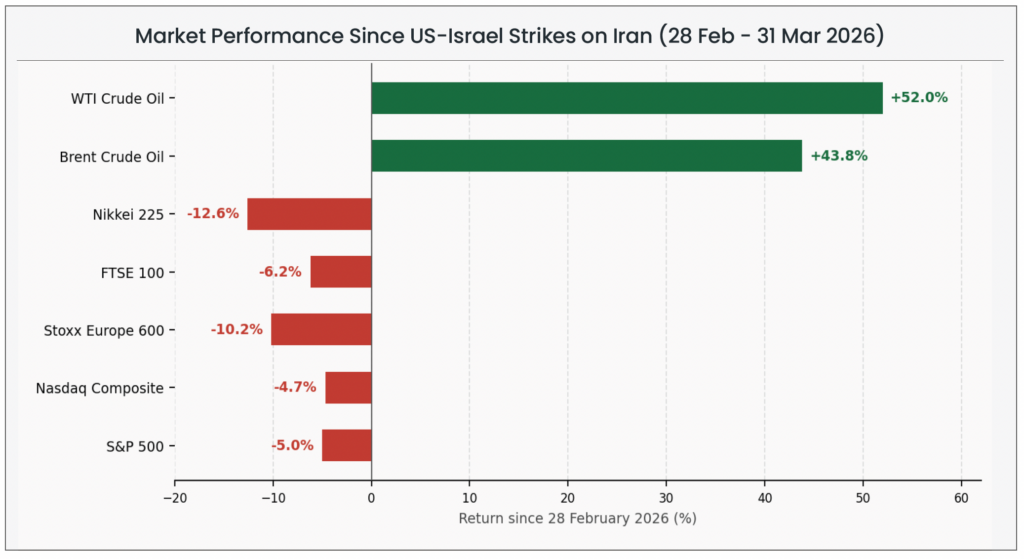

The immediate consequence for financial markets was a sharp surge in energy prices. Iran moved to close the Strait of Hormuz, a narrow waterway through which approximately 20% of the world’s oil supply passes, to all but a handful of vessels. Insurance premiums for ships attempting to transit the strait soared more than twelvefold almost overnight, and several major oil and gas facilities across the Gulf were struck, including Qatar’s Ras Laffan complex, the world’s largest liquefied natural gas (LNG) facility. Brent crude, the international oil benchmark, jumped to as high as $119 a barrel in the opening days of the conflict, up nearly 60% from pre-war levels, before fluctuating between $90 and $115 as attempts at diplomacy and reserve releases calmed markets.

The disruption extended well beyond oil; European gas prices surged 24% in a single session, shipping costs on key global routes rose as much as fourfold, and airlines began drawing up contingency plans for potential jet fuel shortages. Ports in Dubai and Oman were struck by drones, while Iraq closed its oil terminals after tankers off the coast of Basra were hit. The ripple effects reached every corner of the global economy.

Despite some moments of de-escalation, including remarks from President Trump suggesting talks with Iran were progressing, which briefly pushed Brent back below $100, the conflict showed no clear sign of resolution by month-end. Iran’s new Supreme Leader, Mojtaba Khamenei (son of former Iranian leader Ayatollah Khamenei), was appointed within days of the strikes and immediately declared the strait “closed”, signalling that hardline policies were likely to continue. Trump extended his deadline for a peace deal to 6th April, and the US sent a 15-point plan to Tehran via Pakistan, though Iran’s initial response was to describe the terms as “excessive and illogical”. For investors, the overriding message of March was that a prolonged energy shock remained a very real possibility.

Source: Morningstar Direct. Data as of 31/03/2026 (WTI, Brent, Nasdaq, and S&P in USD. Nikkei in JPY. FTSE in GBP. Stoxx Europe in EUR).

Rising energy prices force a sharp rethink on interest rates

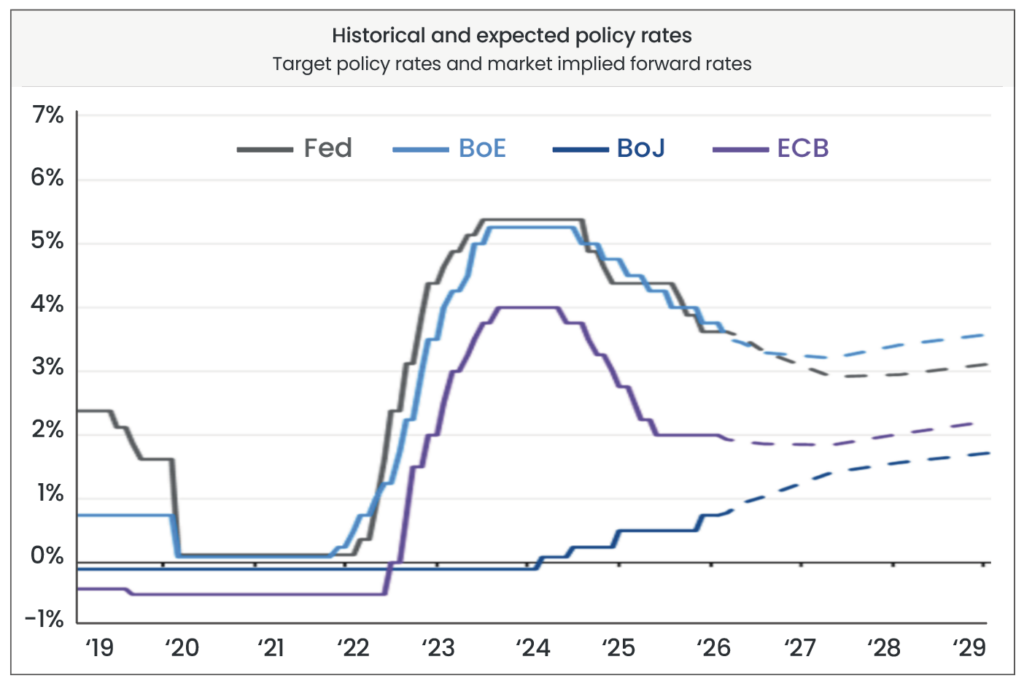

Before the conflict began, the economic backdrop had been broadly supportive of lower interest rates. US consumer price inflation (CPI) had fallen to 2.4%, UK CPI stood at 3%, and eurozone inflation had dipped below the ECB’s 2% target for the first time since 2021. Markets had been pricing in multiple rate cuts across the major economies throughout 2026.

The war in Iran turned that outlook on its head. Surging oil and gas prices are directly inflationary, raising energy costs for households and businesses and feeding through into broader prices. By month-end, market forecasts had shifted dramatically, a sharp reversal from expectations of rate cuts in 2026 just weeks earlier.

Source: Bank of England (BoE), Bank of Japan (BoJ), Bloomberg, European Central Bank (ECB), Federal Reserve (Fed). J.P. Morgan Asset Management (Guide to the Markets). Data as of 27/02/2026.

In March, central banks held firm but sounded the alarm. The Bank of England kept rates at 3.75% but warned a prolonged energy shock could force it to act. UK 10-year gilt yields also surged to 5%, their highest since 2008. The ECB held at 2%, while revising its 2026 eurozone CPI forecast up sharply to 2.6% from 1.9%. The message was clear: the window for rate cuts had closed, and further tightening could not be ruled out.

The UK also faced vulnerabilities, with natural gas accounting for around 35% of total energy supply and significant jet fuel imports from the Middle East. The OBR warned the government was poorly placed to cushion the blow to households, consumer confidence fell to its lowest since last April, and the OECD forecast the UK would have the weakest G7 growth this year, behind only Italy.

For financial professionals only.

Disclaimer

We do not accept any liability for any loss or damage which is incurred from you acting or not acting as a result of reading any of our publications. You acknowledge that you use the information we provide at your own risk.

Our publications do not offer investment advice and nothing in them should be construed as investment advice. Our publications provide information and education for financial advisers who have the relevant expertise to make investment decisions without advice and is not intended for individual investors.

The information we publish has been obtained from or is based on sources that we believe to be accurate and complete. Where the information consists of pricing or performance data, the data contained therein has been obtained from company reports, financial reporting services, periodicals, and other sources believed reliable. Although reasonable care has been taken, we cannot guarantee the accuracy or completeness of any information we publish. Any opinions that we publish may be wrong and may change at any time. You should always carry out your own independent verification of facts and data before making any investment decisions.

The price of shares and investments and the income derived from them can go down as well as up, and investors may not get back the amount they invested.

Past performance is not necessarily a guide to future performance.

What else have we been talking about?

- March Market Review 2026

- Middle East conflict

- February Market Review 2026

- January Market Review 2026

- Annual Market Review 2025

Blog Post by Sam Startup

Investment Analyst at ebi Portfolios