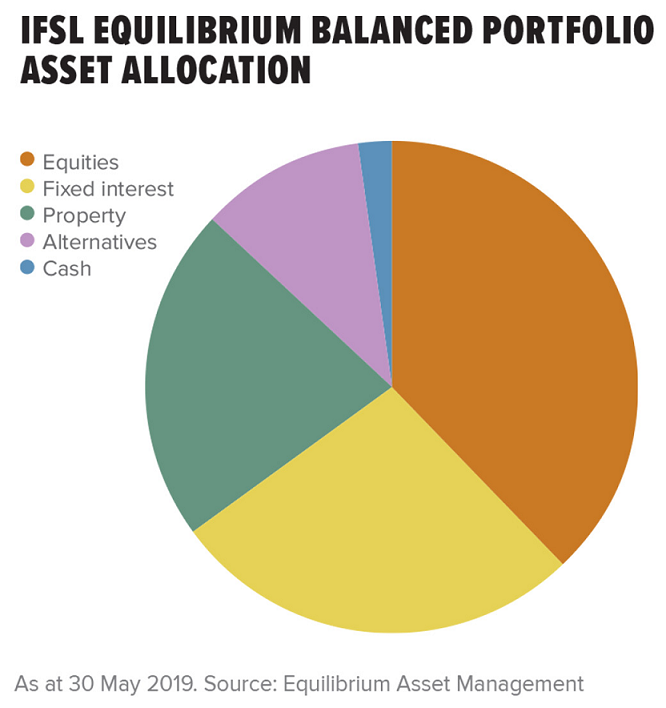

One of the major problems Advisors (and ourselves) face is the expectations of clients. Fuelled by the relentless media focus on outsized gains in some individual assets, (mostly equities), investors imagine that these gains are easily made and thus they should get involved too. The fact is that they are abnormal (or they would not be news at all), but that is not what the media imply. Of course, fund managers are happy to play along, as they judge that this increases the interest in their products and this article contributes to this phenomenon, with the fund manager telling us that Inflation plus 5% is a “realistic and achievable goal”. The chart below does not break down the asset class exposure, but it can be found here.

One or two things jump out – the asset exposure to UK equities is around 14.3%, whilst overseas equity amounts to just under 16% of the portfolio. 20.6% of the assets are in “Alternatives” (Hedge Funds and Infrastructure) and another 14.5% are in Structured Products (mostly Autocall products – see here for a description of what they are).

It is a mystery (to me at least) as to how they expect to make the returns that they imply. Let us look at what implied market return expectations are for various asset classes.

Bonds: the long term return to bonds is simply the yield to maturity; at present, the Global Bond market has a Y-T-M of 1.7% per annum [1]. There are higher-yielding bonds in the marketplace; BBB rated bonds currently yield 3.75%, whilst US High Yield (a.k.a. Junk) bonds have a 6.15% yield, but those returns are subject to (significant) credit risk. The portfolio does own two High Yield bond funds, but most holdings are either very short dated or conventional bond funds. It does own an Index-linked Gilts fund, which has a negative yield, so it is hard to see this area of the portfolio (27% of the total assets) contributing much to this inflation plus 5% goal.

Equities: it is a little more tricky to determine long term returns to equities but broadly, the total expected return can be derived from the formula:

Investment Return (%) = Dividend Yield (%) + Business Growth (%) + Change of Valuation (%).

So, with a current yield on the MSCI World Index of 2.49 %, assuming nominal Long Term World Growth of c.3% and assuming no change in market valuations (P/E/ ratios), gives us an estimate of c.5.5% per annum [2].

But this portfolio is heavily weighted to UK assets, relative to it’s weighting in the World Equity Index (which is 5.8%). Most of the Bond funds are UK focussed, all the Property exposure is the same, the Autocall structured products reference the FTSE 100, alongside a good proportion of the Alternative Equity holdings in addition to the direct UK equity weightings. Summing these gets us to around 49% of the total portfolio (the overall equity content is 73% including Property funds). So we may need to look at return expectations for UK assets rather than those of the World, as they more accurately reflect the potential source of the returns.

The MSCI UK Index dividend yield is currently around 4.5%, with Long Term GDP growth around 2% and as per the document linked to below (p.31), the MSCI UK P/E ratio is 12.4x, which is around the long term average; given the depressed nature of sentiment with regard to UK assets generally, a (downward) change in valuation may be less likely, so an expected return of (4.5+2=) 6.5% may be more secure – though by no means guaranteed.

Putting the bond and equity return elements together, (and allowing for the overall equity/bond allocation), gives us an expected return of (1.7x 27%) + (6.5x 73%) = 0.46+ 4.74= 5.2% per annum – this is nominal and assumes that the UK, rather than MSCI World implied returns are achieved.

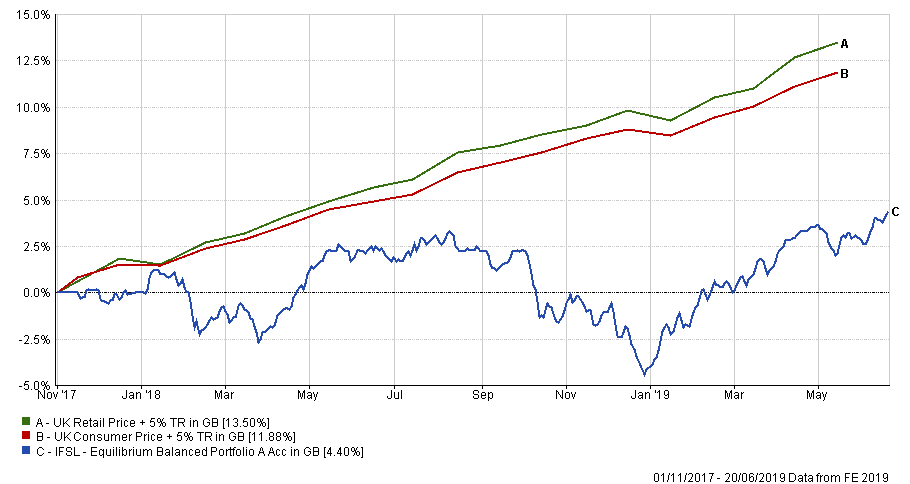

So to meet the Inflation + 5% target, some heroic assumptions (and investments) are going to have to be made; and, as the chart below shows, returns since Inception have been anything but heroic. It has never got close to beating the Inflation plus 5% hurdle – in fact, performance has been akin to CPI +0.5% since 2017. The 1.03% per annum OCF does not help the fund’s chances of achieving the goal, but even if one subtracts the fees, returns since November 2017 would have been +5.7%, still way below the required (or expected) return – a rise in inflation from the current low levels would only make that target more difficult to achieve as stock P/E’s tend to fall in high inflation regimes, as investors require a premium to compensate them for lower real returns (and of course bonds suffer mightily in that environment).

The financial media relentlessly push the idea that outsized gains (such as this), are possible, (even likely), whilst failing to acknowledge the two 17%+ declines in the price (in 2015 and 2018) that would in all likelihood have led investors to sell out. (Note also the start point of the analysis – 2009 marked the absolute lows of the last decade).

Of course, the Equilibrium Balanced portfolio might make their target, but not, as we show above, via their current asset allocation strategy. They will need to take considerably more risk and with that comes the possibility of a Woodford style “blow-up”. Claims such as these will doubtless garner attention (it got ours!), but it is hard enough for Active Managers to outperform Indices in any event, but (some of them) do themselves no favors at all by making wild assertions as to what is achievable. The irony is that, in making these assertions, they are appealing to the very same performance chasing investors that will flee at the first sign that these returns are not being achieved (it is the same short term strategy employed by car Insurance companies – giving discounts to new customers only attracts the same sort of customer that will switch to a better deal the following year!).

In that sense, they are their own worst enemies, leaving investors set up for disappointment, which serves only to drive them towards Index investing. That is where they should be anyway, of course, but it is a bizarre strategy – overpromising and underdelivering, which only serves to undermine further the faith in active investing – if indeed much remains in the light of recent events…

[1] Of course, in the period prior to maturity, bond prices could rise (and thus yields fall) still further, but as the investor will only receive par at maturity and gains above that will be lost, the bond price reverts towards 100 (par), as the expiry of the bond gets closer.

[2] This does require a lot of assumptions, such as that the Long Term Growth rate (I am using GDP as a proxy for business growth), speeds up a little to get back to trend rates of growth and that valuations (with markets at all-time highs) remain unchanged. In the case of the latter, this seems extremely unlikely; the MSCI World Forward P/E is currently 14.6x. Just a 5% drop (to 13.87x) would wipe out nearly all of the expected return. [See page 4 of this pdf to see the long term P/E range for the MSCI World Index, the OECD is a little more gloomy on the longer term trends, however.