February Economic Background

Global equity and bond markets rebounded strongly in February following mixed performance earlier in the year. Equities delivered solid gains as easing inflation in the US and Europe supported investor appetite for risk assets. Fixed income markets also recovered, reversing January’s losses as expectations for interest rate cuts later in the year increased. However, volatility persisted, particularly in the technology sector, where concerns over AI disrupting business models prompted periodic sell-offs. Although markets ended the month on a positive note, the sharp escalation of conflict in the Middle East over the weekend of 28th February/ 1st March highlighted that geopolitical risks remain a key source of volatility.

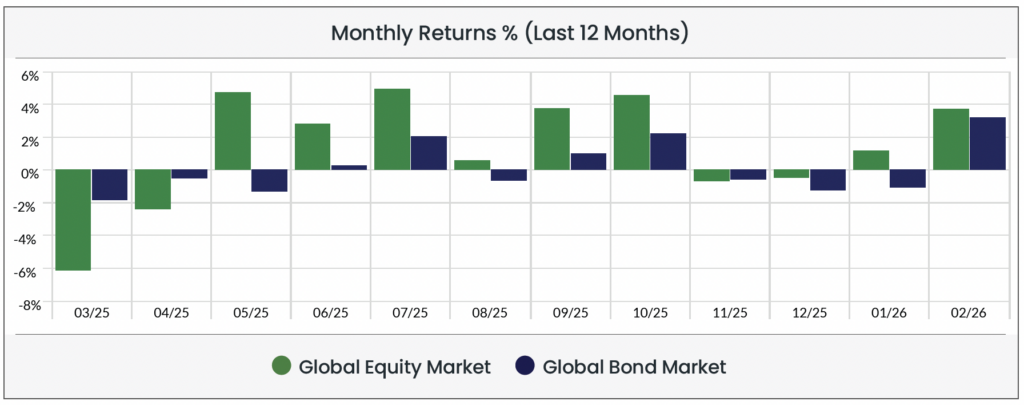

Equity & Bond Performance (Last 3 Months)

Source: Morningstar (Morningstar Global Markets; Bloomberg Global Agg). Data as of 28/02/2026 in GBP terms.

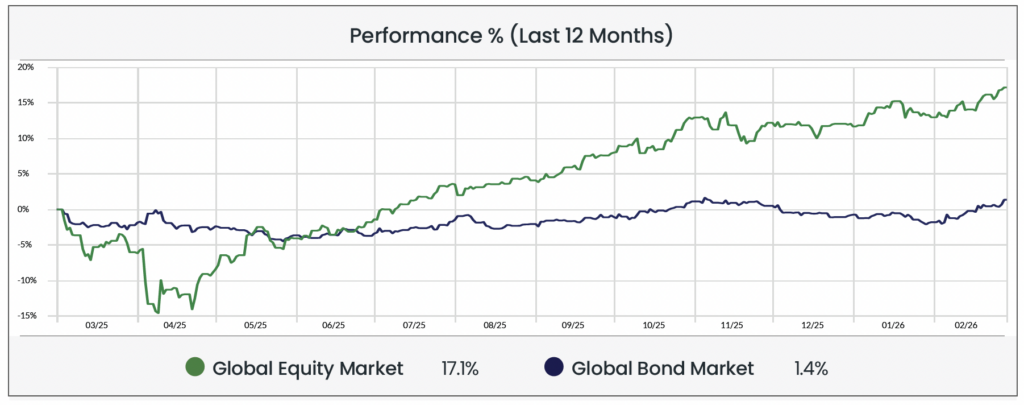

Source: Morningstar (Morningstar Global Markets; Bloomberg Global Agg). Data as of 28/02/2026 in GBP terms.

Source: Morningstar (Morningstar Global Markets; Bloomberg Global Agg). Data as of 28/02/2026 in GBP terms.

Economic Background

Artificial intelligence disruption fuels volatility in technology stocks

Concerns over the disruptive potential of AI were a major driver of market volatility in February, particularly within the US technology sector. Several waves of selling hit software and analytics companies after AI firm Anthropic launched productivity tools capable of automating complex professional tasks such as legal and research work. Investors grew increasingly concerned that rapid advances in AI could disrupt established business models across industries ranging from data analytics to consulting. These concerns triggered a series of declines in technology-heavy indices. The Nasdaq Composite fell on multiple occasions during the month, while the broader S&P 500 also experienced periods of weakness. After a sustained period in which enthusiasm for AI helped drive technology stocks higher, investors are increasingly weighing both the opportunities and risks posed by the technology. While companies such as Nvidia continued to report strong earnings and upbeat forecasts, these results were not always enough to reassure markets, underlining growing caution about the sustainability of the current AI investment boom.

Cooling inflation strengthens expectations of global interest rate cuts

Economic data released during February reinforced expectations that major central banks may continue easing monetary policy throughout 2026. In the United States, inflation fell to 2.4% in January, lower than many economists had anticipated. The data strengthened market expectations that the Federal Reserve could continue cutting interest rates later this year if price pressures continue to moderate. Similar trends were visible in the UK, where inflation declined to 3% while unemployment rose to a post-pandemic high of 5.2%. The combination of slowing price growth and a weakening labour market has increased expectations that the Bank of England could continue lowering interest rates in the coming months. Although policymakers held rates steady during February, investors increasingly interpreted central bank communications as signalling a more accommodative stance ahead. These developments helped support both equity and bond markets during the month. Government bond yields declined from January’s highs as investors priced in a more supportive monetary policy outlook, contributing to the recovery in global fixed income markets.

However, shortly after month-end, tensions in the Middle East escalated sharply. The region remains a critical hub for global energy supply, and any disruption to production or shipping routes can quickly push oil prices higher. Rising energy costs feed directly into inflation by raising input costs for businesses across a wide range of industries. As inflation expectations rise, central banks may be forced to delay or scale back anticipated interest rate cuts in order to prevent price pressures from becoming entrenched. As such, markets have already begun reassessing the outlook for future interest rates, with investors reducing expectations for near-term rate cuts.

Shifting global trade and currency dynamics add to policy uncertainty

Global trade tensions and currency developments remained an important influence on markets during February. US President Donald Trump announced plans to introduce a temporary global tariff on imports, initially set at 10% before being raised to 15%. However, the US Supreme Court ruled that much of the administration’s broader tariff framework was unlawful, creating fresh uncertainty around US trade policy. At the same time, China signalled its ambition to expand the global role of the renminbi, with President Xi Jinping calling for the currency to become a reserve asset. Meanwhile, investors increasingly diversified away from US markets, with European equities seeing record inflows as investors sought to reduce exposure to the concentrated US technology sector.

For financial professionals only.

Disclaimer

We do not accept any liability for any loss or damage which is incurred from you acting or not acting as a result of reading any of our publications. You acknowledge that you use the information we provide at your own risk.

Our publications do not offer investment advice and nothing in them should be construed as investment advice. Our publications provide information and education for financial advisers who have the relevant expertise to make investment decisions without advice and is not intended for individual investors.

The information we publish has been obtained from or is based on sources that we believe to be accurate and complete. Where the information consists of pricing or performance data, the data contained therein has been obtained from company reports, financial reporting services, periodicals, and other sources believed reliable. Although reasonable care has been taken, we cannot guarantee the accuracy or completeness of any information we publish. Any opinions that we publish may be wrong and may change at any time. You should always carry out your own independent verification of facts and data before making any investment decisions.

The price of shares and investments and the income derived from them can go down as well as up, and investors may not get back the amount they invested.

Past performance is not necessarily a guide to future performance.

What else have we been talking about?

- March Market Review 2026

- Middle East conflict

- February Market Review 2026

- January Market Review 2026

- Annual Market Review 2025

Blog Post by Sam Startup

Investment Analyst at ebi Portfolios