“Successful investing is about managing risk, not avoiding it” – Benjamin Graham.

This phenomenon describes the adverse selection / knowledge asymmetry between buyers and sellers in, for example, the used car market. As prices (or in this case, standards) fall, the only willing sellers at a given price will be those that have “lemons” (defective goods) to sell. Thus, the average quality of goods available in the market gradually falls, leaving only poor quality goods left, which is a form of Gresham’s Law.

We at EBI waste no opportunity to lambast high fee charging investment firms (ahem, SJP) – this article I spotted last week was particularly germane to this topic. IPO Wealth is, by its own admission, an “unregistered managed investment scheme, structured as a Unit Trust and based in Australia”. The home page gives a list of Investment Options, offering rates of return ranging from 3.25% (for 3-month investments) up to 6.45% per annum over 5 years. For comparison, here is a list of what is available in Aussie Banks. The rates available on their investments are far in excess of what can be achieved via a bank deposit but there is an extremely good reason for this – what you are investing in, is in no way a deposit!

Once you open an account with them (minimum AUD 100,000, or £53,000), the money is then funnelled towards its parent company, Mayfair 101 (described as a “boutique international investment company”) who then invest it in funding Private Equity transactions. Here is their Factsheet – they are looking for companies that are high growth and on track for an IPO [1] or a trade sale in the next 2-5 years. They take positions in early-stage growth firms via Convertible Notes (which typically pay 10-15% interest rates and have the potential for conversion into equity in the company). How do they manage to obtain such terms? Because such investments are VERY risky.

What makes this SJP-like in its structure, is who gets the up-side and how the risks are distributed; it is exceptionally one-sided. The offer documents state that “… the Unit price (of the investor’s fund) can be less than $1.00 if the Fund’s assets decrease in value but cannot exceed $1.00. The value of your investment is not guaranteed”.

So, should the investments go wrong, the investor is on the hook, but sees almost none of the up-side – compare the interest rates on offer with the 10-15% rates received by the Investment company on the Convertible Notes. This is in no way an adequate compensation for the risks of early-stage investing (but the firm would rather you didn’t focus on that!).

And SHOULD it go wrong, ‘… the Trustee also retains broad discretion to restrict distributions, withdrawals, and redemptions.’ So, there is the risk that one cannot withdraw one’s money either… liquidity risk is not one that would normally be associated with a “term deposit”.

Aside from the obvious – don’t touch this with a barge-pole – what else does it remind us?

1) Risk and return are related (though not always directly); a highly risky asset can generate a higher return but often merely increases overall portfolio volatility if it is not negatively (or lowly) correlated with what is already owned. One thing (return) cannot exist without the other (risk) but investors are constantly bombarded with ideas that purport to offer all the up-side in markets with little (or none) of the downside. Low Volatility strategies are just the latest to show that this idea has risks of its own – just not the ones investors counted on.

{kind=link}

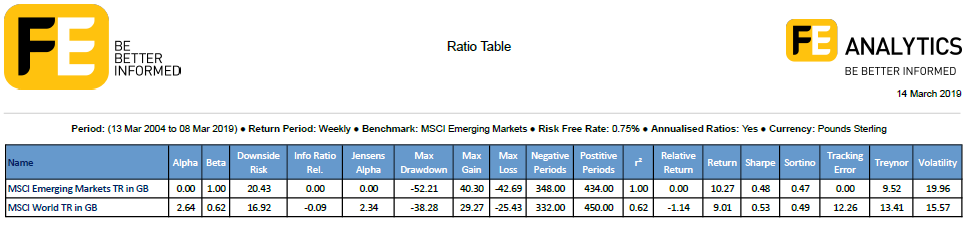

Consider the relationship between Emerging Markets and the rest of the World: as the chart below shows, over the last 15 years, EM has done very well and looks like an obvious way to boost overall returns. But at what cost? RISK.

The table below shows that although returns have been better than that of the MSCI World Index, once adjusted for Volatility (via the Sharpe Ratio), risk-adjusted returns were in fact lower. The same applies if one were to Beta-adjust the returns [2], the EM Index has actually done considerably worse than the MSCI World Index. What looks like a superior return was (mostly) due to taking higher risk.

What risks are investors taking via IPO Wealth? Are they clearly expressed and is the compensation (in the form of returns) commensurate with those risks? In EM, one is aware (or should be) that some Western standards (rule of law, protection of property, etc.) are not as strictly enforced as many would prefer, which is why Emerging Markets equities, for example, tend to be cheaper than their Western equivalents. Global fund flows tend to follow a pro-cyclical pattern, (rising when markets are bullish and falling when risk aversion takes hold). The risks of investing with IPO are not clearly articulated – because if they were, the firm presumably fears that it would get no money!

This is not to say that one should not have risk exposures, but one must consider one’s tolerance (as well as capacity) for risk. At present, the MSCI ACWI (All Countries World Index) has around an 11% weighting in Emerging Markets;- indeed it represents nearly 33% of the World’s GDP, which might imply that it should be higher still. EBI 100 (the closest functional equivalent to the MSCI ACWI), presently has around 13% exposure to the asset class, which can be seen as a compromise between those two positions and as one moves lower down the equity risk scale, that exposure becomes proportionately lower. But we recognise what this exposure can do to overall returns and as such monitor EM fund performance closely.

2) Look carefully under the hood – if something looks too good to be true, it probably is – no “offer” of this sort will be giving anything away for free. In the case of this “investment”, the firm is effectively soliciting low-cost funds in order to invest for themselves in what is effectively Venture Capital funding – with the investor taking all of the risks. The risk profile of the investments being undertaken bare little relationship to that of a cash deposit (which is the fund’s marketing message).

Of course, for many, Due Diligence is a chore and so they do not make the required effort. They probably did not do so with Bernie Madoff, Collateralised Mortgage Obligations and countless other “investment” propositions that ultimately failed either.

But schemes like these remind us of why WE do it.

[1] IPO = Initial Public Offering (i.e. share listing on a stock exchange).

[2] To Beta-adjust returns, divide the Return number by the current Beta and then multiply that by the alternative Index Beta; in this instance, to compare the MSCI World Index return to that of the EM Index, divide 10.27% by 1 and then multiply by 0.62. Thus, if the EM Index had the same Beta-exposure to market risk as the World Index, it would have returned just 6.37%. The higher return was almost entirely due to having higher market risk exposures.

Beta-adjusting returns allow us to compare different risky portfolios on the same basis, to ensure we are getting an apples-to-apples comparison. It allows us to adjust for the amount of (market) risk being taken, as we should expect, for example, a higher risk-weighted (equity) portfolio to do better than a bond portfolio (all things equal).

Disclaimer

We do not accept any liability for any loss or damage which is incurred from you acting or not acting as a result of reading any of our publications. You acknowledge that you use the information we provide at your own risk.

Our publications do not offer investment advice and nothing in them should be construed as investment advice. Our publications provide information and education for financial advisers who have the relevant expertise to make investment decisions without advice and is not intended for individual investors.

The information we publish has been obtained from or is based on sources that we believe to be accurate and complete. Where the information consists of pricing or performance data, the data contained therein has been obtained from company reports, financial reporting services, periodicals, and other sources believed reliable. Although reasonable care has been taken, we cannot guarantee the accuracy or completeness of any information we publish. Any opinions that we publish may be wrong and may change at any time. You should always carry out your own independent verification of facts and data before making any investment decisions.

The price of shares and investments and the income derived from them can go down as well as up, and investors may not get back the amount they invested.

Past performance is not necessarily a guide to future performance.