“Still the man hears what he wants to hear and disregards the rest.” – Simon and Garfunkel (The Boxer).

Ten years ago last week (March 9th, 2009), the S&P 500 hit a low point of 666.79, from which it has subsequently risen to 2,940 in October of last year, for a gain of 441%. A recurring theme throughout this time has been the degree of skepticism, cynicism and general disbelief that accompanied this rise. After a sharp fall into year end 2018, global markets have recovered and currently stand just 3% or so off those highs, as once again, bearish US investors have been “forced in” to the market, as their selling in early January 2019 has led to nothing but frustration.

That this is “the most hated bull market in history” has become a media cliche, (as one can easily see from the number of search results for the phrase). The more interesting question is why?

Clearly one would have only “hated” the current bull phase if one was losing money (i.e. short), but this turn begs the question as to why (some) investors are short (or underweight, which is the nearest an average fund manager can get)? There are many cited reasons for this stance, (over-valuation, the Fed’s interest rate policies, over-elevated profit margins, or as a last resort, a “bubble”). These may or may not be valid, but the deeper cause is likely psychological (or “behavioral”), residing as it does in confidence (or more precisely over-confidence) on the part of these investors.

The problem appears to lie NOT in being wrong about any of these factors per se – we are all wrong about lots of things all the time – but in having too much confidence in one’s forecasts and not updating one’s prior beliefs in the face of non-confirming evidence. When the predicted decline fails to occur or is swiftly reversed, is the market not telling us that the thesis might be wrong? The (clearly strong) confidence in the original hypothesis (for a market crash, major recession or whatever) seems to have been maintained, thus retarding the belief updating process, as evidence to the contrary is ignored or downplayed. Losses thus inevitably accrue (though at least for Hedge Fund managers, they mainly fall on their clients rather than themselves). But fund redemptions DO follow, to their ultimate detriment.

We learn at a young age not to put our hands on a hot stove or in a live electricity socket, but it appears a fair number of investors have not learned the investing equivalent during the last 10 years – at every sign of bad news, a legion of (mainly) hedge fund traders appear willing to aggressively sell (or short) the markets, only to find that they have to cover those short positions (at a loss), pushing the markets higher once again. Of course, the same scenario applies to those waiting on the sidelines – they never seem to find the “right” time to buy, meaning that the longer they wait, the more they miss out on both current and thus future returns.

This phenomenon is known as Confirmation Bias, whereby, once having arrived at a “view” on something people (in this case, Investors) are unlikely to change their minds, even when confronted with new evidence to the contrary. There is no clear connection between intelligence and rational thinking, particularly in the field of investing and the more educated/intelligent one is, the worse this becomes, as they tend to be able to construct seemingly plausible counter-arguments to deflect reality from their Bayesian Priors. As an Oxford Professor, Teppo Felin said, (in a slightly different context), “what people are looking for – rather than what they are merely looking at – determines what is obvious” (to them). Headlines such as this suggest that this bias has not gone away. Indeed, to the contrary, it appears that conviction in a bear market (yet to come) has even been reinforced in what is termed the “backfire effect” (in the realm of politics this may also explain the failure of the US media’s campaign against Trump – it may merely have served to harden his core support. If one doubts the existence of this effect, try telling someone that their house is over-valued!). Feelings about what ought to be, often overrule facts that tell us the way things are. Disbelieving our own arguments is very hard and difficult work, as one Psychology Professor has noted. We often see our opinions as part of our “world view” and thus part of who we are, which may explain our reluctance to part with them, even if it costs us money!

How does this manifest itself in portfolio terms? It may provide a deeper explanation for the returns of two of the Factors we use, Momentum and Value and why they have a negative correlation with each other. If the above provides a good explanation of the failure of investors to revise their beliefs in the face of new information, assets that experience positive news will see further gains (as only gradually do these investors adapt to rising prices, by buying) and thus Momentum will persist; by the same token, for those companies whose news is less positive see a similar underreaction as investors fail to sell out. Thus, both positive AND negative news will not immediately be reflected in prices – so those firms that are doing well see further gains whilst those doing badly see further (relative) underperformance, as, in both cases, Investors fail to “update” their beliefs in the light of new evidence – so Value investors “hold on”, hoping for a recovery whilst Momentum investors hold back, hoping for correction to give them a “better” buying opportunity.

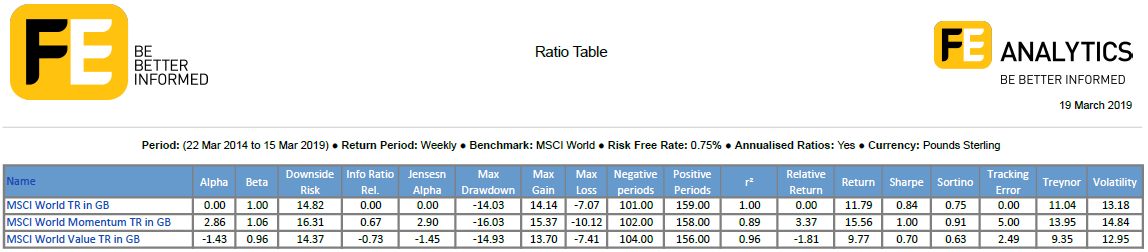

As can be seen in the Ratio Table below, this manifests itself in divergent performance both on a Volatility-adjusted (i.e. the Sharpe Ratio) and on a Beta (market risk) adjusted basis between Value and Momentum [1]. Maybe this situation will change but only once investors accept the situation as it exists (and sell out of the former and buy into the latter). But the degree of tenacity with which these views are (still) being held suggests that this may not happen any time soon. So the phenomenon (for both factors) may well persist.

[1] Both Volatility-adjusted and Beta-adjusted returns attempt to equalise for differences in portfolio structure; in the former case, it measures the per-unit return for each unit of risk (assumed to be proxied by Volatility of returns) and in the latter by market (i.e. Beta) risk being taken. This enables one to compare differently risky portfolios/assets/Indices on an apples-to-apples basis.

{kind=link}