“Truly, the real black swan problem of stock market busts is not about a remote event that is considered unforeseeable; rather it is about a foreseeable event that is considered remote. The vast majority of market participants fail to expect what should be, in reality, perfectly expected events.” Mark Spitnagel, The Dao of Capital.

This applies equally well to ALL assets, not just stocks.

Some of the most malign consequences of QE, ZIRP, NIRP[1] and so on have fallen on savers. It is now practically impossible to live off the interest from savings (unless you are Donald Trump, in which case you’re a bit busy at the moment), which forces Investors to “Reach For Yield”, with potentially dangerous implications. However, they are not the only victims- Pension Funds are under assault on two fronts, one more technical, one very practical.

The technical one is due to the way they value their assets and liabilities, thus providing a snapshot of their solvency [2]. As discussed below, the fall in Interest Rates has an immediate and negative impact on the fund’s solvency position.

The second is related to the first-how to successfully invest in order to achieve their ultimate objective, namely, satisfying their financial obligations to their members. Last week, as Blomberg reported , Ireland sold 100 year bonds at just 2.35%- below the yields of comparable US Treasuries (!). As Pension Funds invest heavily in Fixed Income securities, this is lowering returns and/or forcing them to take more risk as the OECD has warned. Hedge funds, Private Equity and other “Alternative Assets” now constitute 10-15% of their Portfolios, helping to justify their elevated expected rate of return assumptions- the higher the assumption, the lower the actuarial deficit, so optimism is helpful to plan sponsors. In the US , CalPers, the Californian Public Sector Pension Scheme recently reduced their Expected Rate of Return from 7.75% p.a to 7.5% p.a, but is this realistic even now ? Assuming a 60:40 equity/bond allocation, with Bonds now yielding 1.74%, the non-Bond element will have to earn 11.34% annualised in perpetuity! [3] to achieve that target.

Of course, Interest Rates may rise, but regardless of the proximate cause, what will this do to non-bond assets? If one rate rise can do somuch damage to markets (see below), it does not inspire confidence in their resilience to several rises. Equity assets are thus vulnerable to “re-valuation” risk which may offset all of the Discount Rate benefits accruing from a rate rise. For Pension funds, this may be a case of “be careful what you wish for”.

Sooner or later, this will start to erode Pension plans. The death of Private Sector DB (Defined Benefit) plans has been well documented, but has become topical again in the light of the troubles facing BHS and more recently Tata Steel , both of which have substantial pension fund deficits which are inhibiting their restructuring.

It is now impinging upon the Public Sector too. Slowly but surely, they to are being forced to confront reality- in the US, the situation in Detroit has been on-going for months, but now Kansas retirees are about to see 50%+ cuts in benefits, or face total bankruptcy of the fund. In addition to the Puerto Rico saga (first mentioned here in July 2015), we now have problems emerging in New Jersey[4], and in Chicago, all of which has led to sharp falls in Municipal bond prices and sharp downgrades in their credit ratings. This article suggests Puerto Rico’s next move is capital controls, which wont be greeted favourably by their bondholders.

Raising taxes is not a long-term option: it merely leads to people moving out of the area. Detroit has lost 50% of its peak population since the 1950’s , and that of Chicago has (as of 2014) fallen below its level of the 1920’s. There is no reason to assume residents will be any more wiling to accept this in the UK either- it just hasn’t happened here yet.

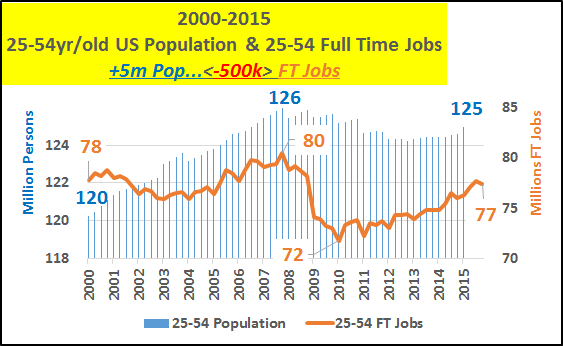

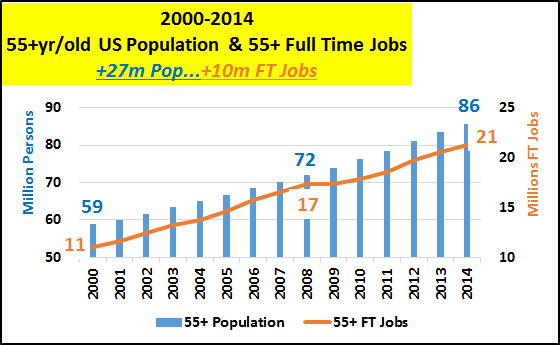

One of the consequences of the reductions in expected returns from pensions is that the older generation are delaying retirement, thus filling jobs that would otherwise go to the young (see charts below). The raised demand for employment keeps wage growth down, which in turn keeps inflation in check, reducing the need to raise interest rates.

If this all seems somewhat circular in nature, it’s because it is.

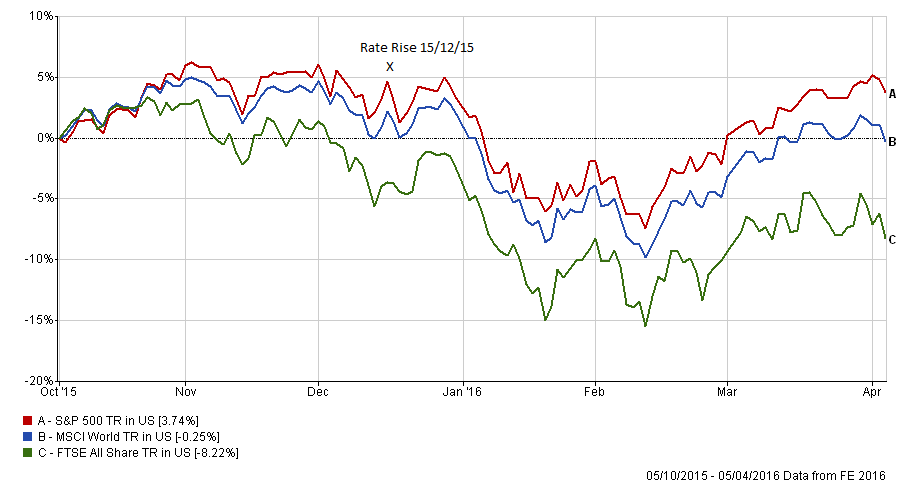

The flow chart below illustrates the dilemma Central Banks (particularly the Fed) are in. In truth, they have created it themselves. It should be good for most assets, especially Bonds, but it appears to be creating instability. This might explain the seemingly perpetual state of Bubble and Crash that we have witnessed over the last few years. We have had 3 “crashes ” since October 2014 leaving the markets little changed (the MSCI World Index is -2.6%, the S%P 500 +3.5% since October 2014).

Lest this should sound like a counsel of despair, let us note that it is by no means pre-ordained. But it does suggest that one should not place too much faith in any one asset. Stay diversified and stay away from “risky” bonds, esoteric US Municipal Bonds for example (investors are now finding out why they are tax-free-because there is little likelihood of achieving a taxable gain !). It also highlights that the clamour for investors to sell bonds last year was looking at the wrong sector of the bond market, and that worries about extended equity valuations may be a function of the market’s understanding of these bond market risks.

Rationalisations, like hindsight, are perfect, but investors have to deal with the future. We stick to the same theme- high quality bonds dilute the risks associated with owning equities. We know of no-one who can successfully switch between them, so we will aim to own as many different assets as possible, re-balancing as necessary.

If you still crave excitement however, open a law firm in Panama…

[1] Quantitative Easing, Zero Interest Rate Policy, Negative Interest Rate Policy.

[2] As an example, the West Yorkshire Pension Fund annual report for 2014/15, reports a funding deficit of 18.9% for 31/3/13 (page 76), assuming a Discount Rate of 4.5%. QE has pushed that Rate lower, thereby raising the liabilities and increasing the reported deficit.

Imagine a Pension fund with Assets of £50 and Future liabilities of £100 due to beneficiaries. Assuming an average retirement date 15 years in the future, the net liability would be £50/ 1.045¹⁵ = 50/1.9352. This gives a Present Value of the Obligation of £25.83.

But if the Discount Rate falls to 3%, the Liability rises; £50/ 1.03¹⁵ = 50/1.5579= £32.09. This may not seem like much until one multiplies the numbers by several hundred millions of Pounds…

A fuller discussion of the process of Pension Fund valuation can be found here .

[3] (60% x 11.34 +(40% x 1.74)= 7.5% p.a.

[4] According to Bloomberg, “New Jersey relies on personal income taxes for about 40% of its revenue, and less than 1% of taxpayers contribute about a third of thosecollections. A one percent forecasting error in the income-tax estimate can mean a $140 million gap.” So the departure of just ONE Billionaire is a big deal.

Disclaimer

We do not accept any liability for any loss or damage which is incurred from you acting or not acting as a result of reading any of our publications. You acknowledge that you use the information we provide at your own risk.

Our publications do not offer investment advice and nothing in them should be construed as investment advice. Our publications provide information and education for financial advisers who have the relevant expertise to make investment decisions without advice and is not intended for individual investors.

The information we publish has been obtained from or is based on sources that we believe to be accurate and complete. Where the information consists of pricing or performance data, the data contained therein has been obtained from company reports, financial reporting services, periodicals, and other sources believed reliable. Although reasonable care has been taken, we cannot guarantee the accuracy or completeness of any information we publish. Any opinions that we publish may be wrong and may change at any time. You should always carry out your own independent verification of facts and data before making any investment decisions.

The price of shares and investments and the income derived from them can go down as well as up, and investors may not get back the amount they invested.

Past performance is not necessarily a guide to future performance.

User & Cookie Notice

This website is for Financial Advisers, Paraplanners and Financial professionals only.

By clicking the acceptance button below, you confirm that (a) you are a financial adviser, paraplanner or financial professional AND (b) you have read the website terms of use and agree to be bound by them.

Cookie Notice

Some cookies are essential, while others help us improve your experience by providing insights into site usage.