“The Americans will always do the right thing… after they’ve exhausted all the alternatives” . (attributed to Churchill, though there is doubt as to its veracity).

The row between the US and North Korea has been escalating, with increasingly angry words and threats (whose intensity is mirrored 5000 km away on the Indo-Chinese border) being exchanged. After studiously ignoring the rise in the diplomatic temperature for nearly a month, last week it suddenly exploded into life with markets, especially Asian markets, understandably taking fright. Buying resumed this week as nuclear Armageddon didn’t occur over the weekend, (though one must wonder who these “investors” think they will be able to sell to in the event of a holocaust), but the situation remains tense as both sides contemplate their next moves.

Donald Trump (inevitably) started the proceedings [1] with a threat to launch “fire and fury” should North Korea launch any “aggression” prompting an immediate reaction from North Korea (NK), stating that “sound dialogue is not possible with such a guy bereft of reason and only absolute force can work on him,” (which brings to mind kettles and pots), accompanied with the threat that they were “seriously examining” a plan to strike at Guam (here’s where it is), with mid-August the putative deadline for it’s implementation. This has now passed, but the door is still open, should Kim Jung Un decide to call Trumps’ bluff.

{kind=link}

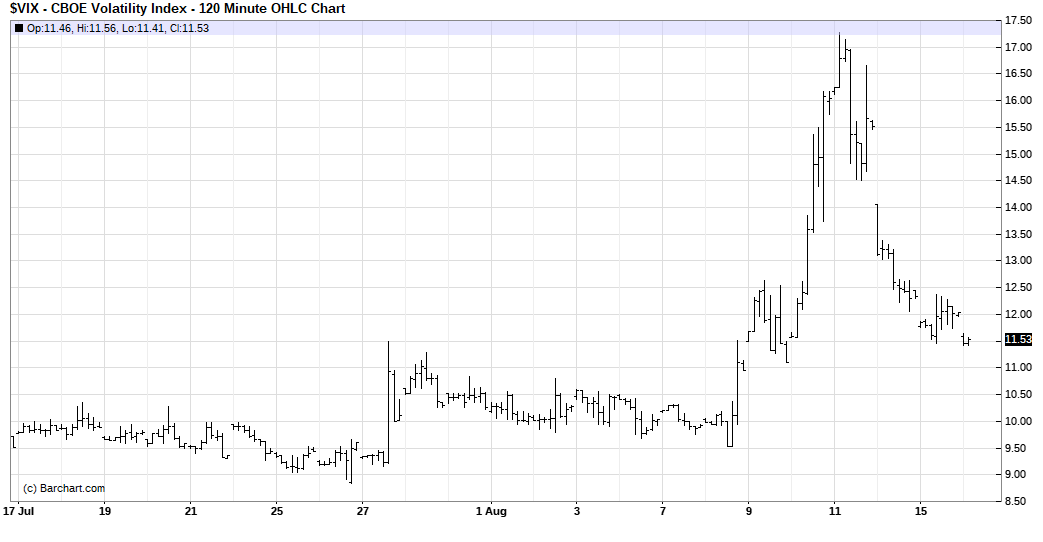

So far, all the market action has been in the VIX (Volatility) Index with the price going vertical last week, though it has now backed off a bit. The S&P 500 is less than 2% from its all time highs so, for now, investors are still sanguine [2].

Americans appear to be worried, with 62% of those surveyed asserting that NK poses a “serious threat” to the US, up from 48% in March according to a CNN poll. 50% of those asked want the US to take “military action”. Parallels have already been drawn with the Cuban Missile Crisis of 1962, but this appears different, if only because it was widely believed at the time that Khrushchev didn’t want nuclear war either. It is not clear that the same certainty exists with Kim Jung Un. Since neither side is likely to back down easily, how this is resolved is hard to tell. But we can see a number of factors that inhibit both actors from overplaying their hands;

Both are more constrained in their freedom of action than they would like the world to believe;

– Trump risks looking foolish should his chosen course of action backfire, which would destroy his political credibility. For Kim, that same result could easily lead to his death- the pictures of Qaddafi in Libya, bedraggled and terrified after his overthrow, shows the personal risks Kim faces from seeming weak, or incompetent.

– Would Trump want to use nuclear weapons on a country that borders both Russia AND China? Alternatively, should NK launch missiles on Guam, and the US THAAD missile defense system shoots them down, NK would be deeply embarrassed and Kim may find his support base severely compromised.

– With both the Russians and the Chinese looking on, both would gain an enormous strategic benefit of being able to see the US system in action, whether it succeeds or not; either way, they learn a lot about US military capabilities.

Thus, neither side has much to gain from going to war (and quite a lot to lose), so it is likely that bluster may be the only thing they can get away with. But it could go on a lot longer than most people either expect or desire.

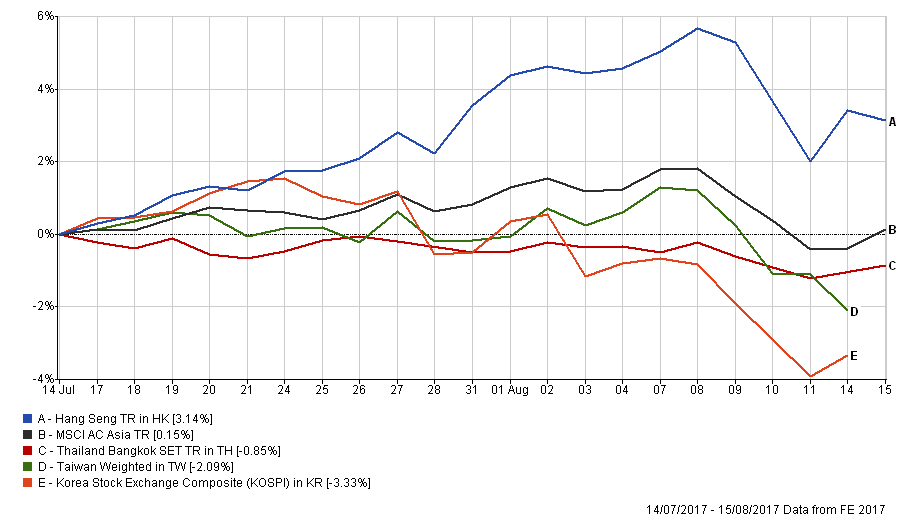

What to do? As usual for us, the answer is nothing. Emerging-market assets have been the rampant out performers of 2017. The macro fundamental arguments for the vast majority of these assets remain in place: solid growth, high real yields, very cheap currencies, great demographics, an exploding middle- class and exposure to a consistently growing Chinese economy . These are long term factors, though, and will be of no help should war actually break out; during acute periods of risk-aversion, positioning dominates fundamentals, as those who are long (in this instance), try to reduce exposures, while those short will await developments. This is why some of the best structural investment stories can see the most painful corrections in the short-term. Furthermore, the relatively illiquid nature of EM not to mention the costs of buying and selling make it very hard to exit quickly, particularly if other players are trying to do the same. In the 20 years to 2016, nearly every calendar year has seen a 10% MSCI EM Index correction at some point, so it is a feature not a bug of the market ecosystem in those markets.

If one does sell, when to get back in? The lessons of failed attempts at market timing are all too clear and it is a losing proposition for most if not all investors. EBI Vantage portfolios recently completed a re-balance, selling EM to buy bonds (mainly), not because we saw this coming (we didn’t), but to maintain target weightings and thus diversification requirements.

What Kim or Donald do in the future will not change that approach, (or at least not in a way that could be responded to!). In the meantime, life goes on…

.

[1] After yet another series of ICBM missile tests in June and July.

[2] It will be instructive to see how far Trump pushes this. After all, he has recently attempted to take credit for the rise in the stock market, so a crash would not look good at all- will the Stock Market be the ultimate arbiter of how far he can go?

Disclaimer

We do not accept any liability for any loss or damage which is incurred from you acting or not acting as a result of reading any of our publications. You acknowledge that you use the information we provide at your own risk.

Our publications do not offer investment advice and nothing in them should be construed as investment advice. Our publications provide information and education for financial advisers who have the relevant expertise to make investment decisions without advice and is not intended for individual investors.

The information we publish has been obtained from or is based on sources that we believe to be accurate and complete. Where the information consists of pricing or performance data, the data contained therein has been obtained from company reports, financial reporting services, periodicals, and other sources believed reliable. Although reasonable care has been taken, we cannot guarantee the accuracy or completeness of any information we publish. Any opinions that we publish may be wrong and may change at any time. You should always carry out your own independent verification of facts and data before making any investment decisions.

The price of shares and investments and the income derived from them can go down as well as up, and investors may not get back the amount they invested.

Past performance is not necessarily a guide to future performance.