“The things that will destroy America are prosperity-at-any-price, peace-at-any-price, safety-first instead of duty-first, the love of soft living, and the get-rich-quick theory of life” – Theodore Roosevelt.

As we discussed last week, professional investors (a very loose term), are remaining bearish on US equities, but they are by no means alone. In this market cycle, far from becoming euphoric, investors are becoming ever more concerned/worried/anxious as prices rise higher. It IS an unusual state of affairs and heightened by the financial media’s constant doom-laden headlines; sometimes it appears that investors won’t fully relax until there’s a crash!

What we can do is to try to discern why it is that the US has crushed the bears and roared ahead of other markets, as it has for the last 5 years [1] and whether American markets represent a major risk to the investor. There appear to be three sources of risk for the investor – politics, economics and market positioning, but as we went through some of the causes of this “institutional bearishness” last week, it is not necessary to reprise the third of these.

It is fashionable to regard Donald Trump as “dim”, “erratic” and “impulsive”, though as neither I nor I imagine many other British “opinion formers” have met him, this view appears to come mainly from the UK media (only some of whom have met him either). There has been a pattern established since the 1980s whereby Republican Presidents (Reagan, Bush – one and two – and now Trump) are portrayed as buffoons, whereas the foibles of Democratic Presidents are downplayed or overlooked altogether – but who exactly is creating this narrative? A left-leaning mainstream media (MSM) cabal, such as CNN, CBS, MSNBC and newspapers such as the (Amazon-owned) Washington Post, etc. who absolutely hate Trump with no equivocation. They have not and will not forgive him for the “sin” of successfully winning the election ahead of their acclaimed favourite Hilary Clinton. Sadly, it seems that UK outlets merely parrot this opinion, (largely because they have a similar world view). Is he stupid, or does he just have a different modus operandi? Different does not equal worse (or dumber!) and at least for now, the trade war threats appear to have worked with Mexico and may still work with China too, (though that is harder to see happening anytime soon), but it represents a major change in the US approach to other nations and an increased willingness on the part of the President to use a more confrontational strategy – if it works, he (and his voting base) will be happy.

Whether one prefers this attitude is not relevant, but either way it is very dangerous to base an investment strategy on one’s political view; markets don’t care what we think about politics (or much else either); they move on a multitude of factors, only one of which may be politically focussed. To concentrate ones’ investments on a (political) view of one person is to miss the other variables that contribute to market moves. It is best to keep one’s politics separate from one’s portfolio or risk losing money for reasons that have nothing to do with investing. It is hard enough to make money in markets without tying ones financial fortunes to an ideology of any sort.

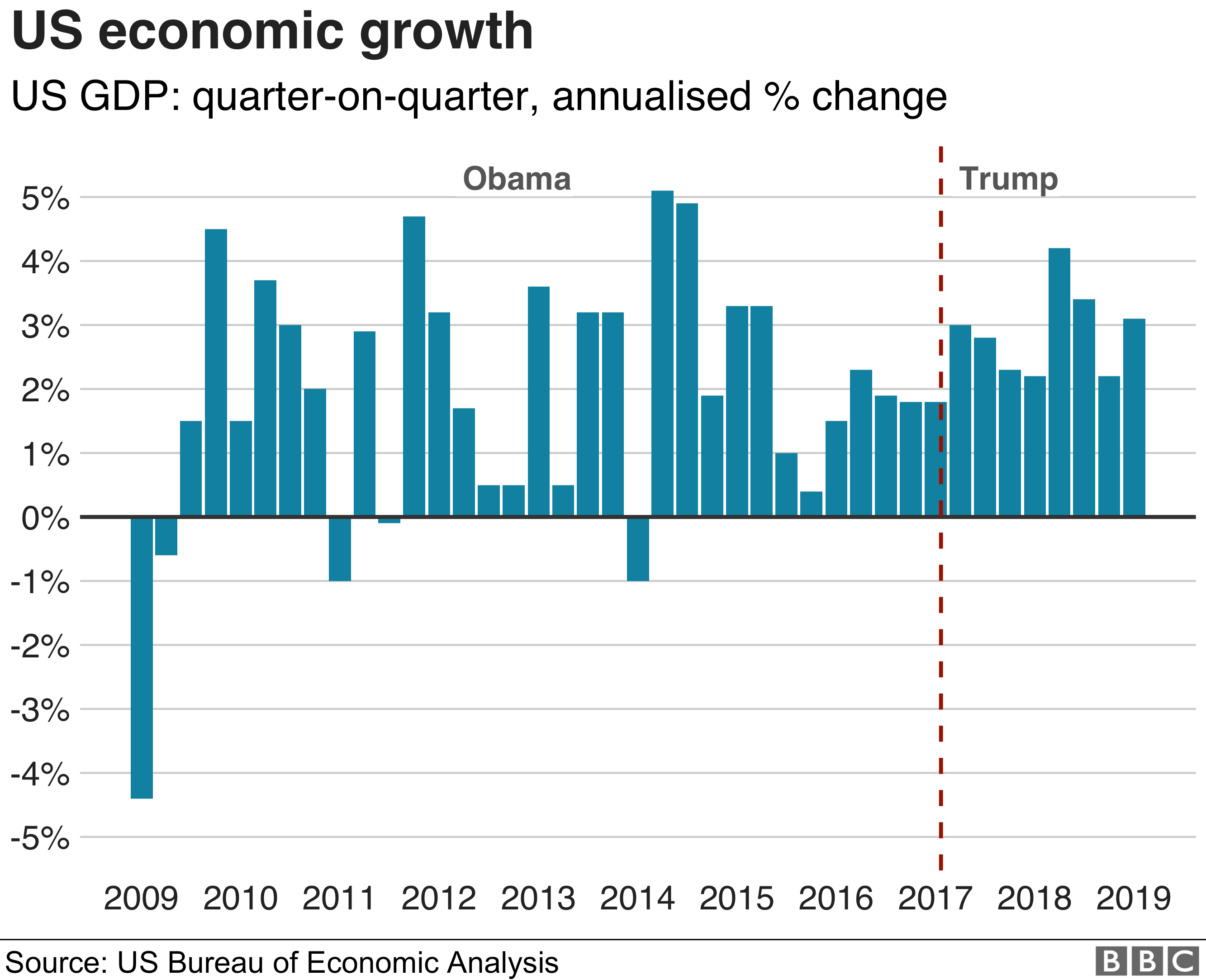

What of economics? US economic growth has been mostly above 2.5% under Trump’s presidency, which although not spectacular, has been far better than Europe, Japan and that of Blighty, to name but a few [2]. It is widely held that the US economy is in the “late cycle”, which is another way of implying that a recession is close. So, if we assume economists are correct – an inherently dangerous view to take, given their track record – the economy will soon go into reverse, with profit warnings, investment sell recommendations and falls (maybe sharp ones), in share prices.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

But what will happen elsewhere in the World? Near zero interest rates already prevalent across European and Japanese markets and the rise of negative yielding bonds across the globe are not a sign of strength – the opposite in fact. If the US falls into recession, the rest of the world will inevitably follow, as they are hugely dependent on the US for export revenue. As share prices fall, correlations between international markets tend to rise, meaning that falls in the US will inevitably translate into market falls elsewhere and volatility will thus increase; markets elsewhere are cheaper than the US but for a reason – when things go wrong, they are worse for EM/Europe and Japan due to their reliance on selling goods to the US. The problem for the rest of the world is that they have become a “derivative” of the US, utterly dependent on the latter for their own growth, which is why competitive currency devaluation is once again becoming the policy of choice, which the President has pointed out (more than once). So, how “safe” would selling out of the US actually be? The short answer is, not very – if the US economy falls, other economies will do the same and the latter will NOT recover until there are signs of the US doing so too. The idea of “decoupling” between the US and global stock markets is a myth in a globalised world and until the likes of Germany, China, and Emerging Markets generally, develop an economic model that relies on domestic consumption rather than mercantilist policies to create growth, that will remain the case.

{kind=link}

{kind=link}

.png)

So, what is to be done? In short, nothing. Given that the US stock market capitalisation has a 60% weighting in the MSCI World Index, (the UK has a 6% weighting), it would be extremely risky to be underweight the US to any significant extent. This would be the converse of the UK Bias problem that has confounded investors for the last 5 years – an overweight to the UK (or underweight to the US), would be a major “bet” on relative returns (of either market), one that neither we nor anyone else can be confident of getting right.

The chart above shows the 5-year performance of the S&P 500 and the FTSE All Share (as proxies for the US and UK equity markets), with the MSCI World as the investment return one would have achieved by investing on a market-cap basis. Let us suppose that one had a £100 portfolio with weightings of 31% and 12% (i.e halving the US and doubling the UK exposure respectively). The US exposure would have returned (31 x 2.2128 =) £68.60 and the UK assets (12 x 1.3643=) £16.37, giving us a return of £84.97 from these two markets. But leaving them at MSCI weights gives the investor a return of (62 x 2.2128 + 6 x 1.3643) = £145.37, 70% more than the alternative asset allocation. Mathematically, the UK would need to outperform by more than six times the US for this trade to work!

This is, of course, what HAS happened and not necessarily what WILL do so, but in the absence of a crystal ball, we should stick to the plan. No amount of information will necessarily be of any use though, as those who correctly foresaw the victory of the UK “Leave” campaign or who predicted Donald Trumps’ election would not have made any money, as both were perceived as bearish events. So, one needs to know how market participants react to that news as well as the news itself. There is a ready market for such soothsayers, but they tend to make more out of their predictions than do their audience…

[1] In the chart above, all four Indexes are MSCI World minus one market region. If they are above the MSCI World Index return, it implies that those markets (Europe and the UK) have been a drag on overall Index returns whilst the US has been a net contributor to the MSCI World Index as the ex-US Index is below the overall Index; it this instance, the chart suggests that 42.5% of the total MSCI World Index return over the last 5 years has been due to the US markets (50.59/87.96-1 = 42.485).

[2] In truth, however, sitting US Presidents have a relatively small influence on the economy as a whole (due to the checks and balances in their political system). They can, of course, do harm, but the incumbent can only really influence events – the Fed is a much bigger fish in the economic pond, which is why Trump is relentlessly badgering them about interest rates, the Dollar and anything else he can think of – he knows where the real power lies.

Disclaimer

We do not accept any liability for any loss or damage which is incurred from you acting or not acting as a result of reading any of our publications. You acknowledge that you use the information we provide at your own risk.

Our publications do not offer investment advice and nothing in them should be construed as investment advice. Our publications provide information and education for financial advisers who have the relevant expertise to make investment decisions without advice and is not intended for individual investors.

The information we publish has been obtained from or is based on sources that we believe to be accurate and complete. Where the information consists of pricing or performance data, the data contained therein has been obtained from company reports, financial reporting services, periodicals, and other sources believed reliable. Although reasonable care has been taken, we cannot guarantee the accuracy or completeness of any information we publish. Any opinions that we publish may be wrong and may change at any time. You should always carry out your own independent verification of facts and data before making any investment decisions.

The price of shares and investments and the income derived from them can go down as well as up, and investors may not get back the amount they invested.

Past performance is not necessarily a guide to future performance.